Ask ten finance professionals to define “sustainable investment” and you’ll likely get ten different answers. Some will describe ESG screening. Others will talk about impact funds or green bonds. A few might cite the UN Sustainable Development Goals. This confusion isn’t just semantic. It shapes how funds are structured, how products are marketed, and how regulators evaluate compliance. For finance professionals and students building careers in this space, getting these definitions right is foundational. This article breaks down the regulatory definitions, key methodological differences, performance evidence, and practical frameworks you need to work confidently in sustainable finance.

Table of Contents

-

ESG, impact, and sustainable investing: Key differences and approaches

-

How sustainable investing is implemented: Methodologies and measurement

-

Sustainable investment performance: What the evidence really shows

-

What most guides miss: Why nuanced ESG analysis trumps labels

Key Takeaways

| Point | Details |

|---|---|

| Sustainable investment definition | It means targeting measurable social or environmental benefits and not doing harm to other objectives. |

| ESG vs impact investing | Impact investing requires measurable real-world outcomes and active investor involvement, beyond ESG integration. |

| Many approaches exist | Sustainable investing is not one-size-fits-all and uses multiple methodologies and rating systems. |

| Performance varies by strategy | Research shows sustainable investments do not consistently outperform or underperform traditional benchmarks. |

| Scrutinize methodologies | Understanding rating and measurement models is crucial for authentic ESG analysis and portfolio decisions. |

Defining sustainable investment: More than just a buzzword

The term “sustainable investment” gets used loosely in marketing materials, fund prospectuses, and media coverage. But in regulatory contexts, it carries a specific and demanding meaning. Understanding that distinction is the first step toward genuine expertise.

Under the EU’s Sustainable Finance Disclosure Regulation (SFDR), sustainable investment has a precise definition tied to generating clear, measurable social and/or environmental benefits while not doing significant harm to other objectives. This isn’t a soft requirement. Funds classified as Article 9 under SFDR, sometimes called “dark green” funds, must demonstrate that their investments meet this standard. That means evidence, not just intention.

“Sustainable investment” in EU regulatory usage requires generating clear measurable social and/or environmental benefits and not doing significant harm to other objectives. It is not enough to simply avoid harmful activities; funds must actively demonstrate positive contribution.

This matters enormously for practitioners. A fund that excludes tobacco or weapons manufacturers is not automatically a sustainable investment under SFDR. Exclusion is a starting point, not a destination. The “do no significant harm” (DNSH) principle requires that each investment be assessed across all six environmental objectives defined in the EU Taxonomy, covering areas from climate change mitigation to biodiversity protection.

Why does this confusion persist? Partly because “sustainable” is used in everyday language to mean anything from “long-term” to “eco-friendly.” In finance, the word has been stretched to cover everything from light ESG screening to full-impact strategies. Many fund managers use the label without the regulatory rigor. Professionals who understand the regulatory baseline are far better positioned to evaluate products, advise clients, and build compliant strategies. Exploring sustainable investment courses that cover SFDR and EU Taxonomy frameworks is one of the most direct ways to build that foundation.

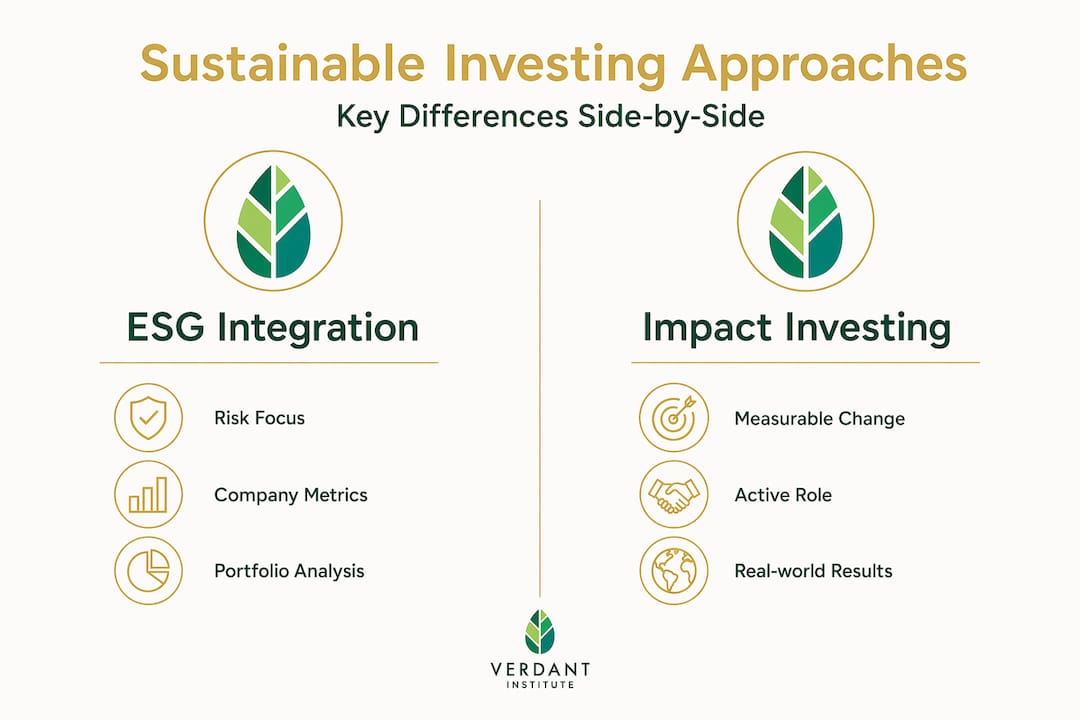

ESG, impact, and sustainable investing: Key differences and approaches

With a regulatory definition in mind, let’s explore how sustainable investment overlaps with, and differs from, both ESG and impact investing. These are related but distinct concepts, and conflating them creates real problems in product design, reporting, and client communication.

ESG integration focuses on incorporating environmental, social, and governance factors into investment analysis and portfolio construction. The primary goal is financial materiality: identifying risks and opportunities that affect returns. An ESG-integrated portfolio may hold companies with significant carbon footprints if those companies are actively managing transition risk. The process is analytical. There is no requirement for active real-world outcomes. ESG data informs the investment decision, but the fund is not obligated to demonstrate that its holdings are generating measurable positive impact.

Impact investing operates differently. It requires a theory of change, measurable real-world results, and active investor engagement. Impact investing adds a requirement for measurable real-world outcomes and an active investor role, beyond simply considering ESG factors. This means the investor must be able to demonstrate that their capital contributed to a specific outcome, such as reducing carbon emissions by a quantified amount or improving access to healthcare in an underserved community.

Sustainable investing sits between these two, depending on the framework. Under SFDR, it requires positive contribution and DNSH compliance. Outside of SFDR, it is often used interchangeably with ESG integration, which is precisely where the confusion begins.

There is no single monolithic methodology; investors implement sustainable investing via multiple approaches that differ in objective and mechanics. Understanding categorizing sustainable investing approaches and how they map to regulatory frameworks is essential for anyone designing or evaluating investment products.

| Strategy | Primary goal | Outcome requirement | Active engagement |

|---|---|---|---|

| ESG integration | Financial risk/return | No | Optional |

| Sustainable investing (SFDR) | Positive contribution + DNSH | Yes, measurable | Required at fund level |

| Impact investing | Measurable real-world change | Yes, verified | Required |

| Exclusion/negative screening | Values alignment | No | No |

| Thematic investing | Sector exposure | Partial | Optional |

Key distinctions to keep in mind when evaluating any fund or strategy:

-

ESG integration does not guarantee positive environmental or social outcomes

-

Impact investing without additionality (the idea that the investment caused the outcome) is not genuine impact

-

Sustainable investment under SFDR requires documented evidence, not just a label

-

Thematic funds (clean energy, water) may or may not qualify as sustainable under regulatory definitions

Pro Tip: Be wary of strategies that market themselves as “impact” without specifying an active investor role or providing a documented theory of change. Real impact investing is verifiable. If a fund cannot tell you exactly what outcome it is driving and how it is measuring that outcome, the label is likely marketing rather than methodology. You can also explore approaches to trading and investing across different asset classes to see how sustainable strategies compare in practice.

How sustainable investing is implemented: Methodologies and measurement

Having mapped out the approaches and definitions, it’s time to look at how institutions and asset managers implement and measure sustainable investing day-to-day. The mechanics matter because they determine what you’re actually buying when you invest in an ESG or sustainable fund.

Implementation generally follows two broad orientations. Top-down approaches start with macro-level themes or sector allocations, then filter down to individual securities. A top-down manager might allocate to clean energy as a theme and then select the best-performing companies within that sector. Bottom-up approaches start with company-level ESG analysis and build portfolios security by security based on individual scores or assessments. Most institutional asset managers use a combination of both, but understanding the dominant approach tells you a lot about how a fund’s ESG credentials are constructed.

At the fund level, ESG ratings are the most widely used measurement tool. MSCI ESG Fund Ratings translate underlying holdings’ ESG scores into fund-level scores using a specific calculation approach that weights each holding’s score by its proportion in the fund. Here’s how that process typically works:

-

Assign an ESG score to each underlying holding based on company-level ESG data

-

Weight each holding’s score by its portfolio weight

-

Aggregate weighted scores to produce a fund-level ESG score

-

Adjust for coverage (what percentage of holdings have ESG data)

-

Apply a rating scale (AAA to CCC in MSCI’s case) based on the final score

This sounds straightforward, but the complexity lies in step one. How does MSCI score a company? It uses industry-specific key issues, assessing exposure to ESG risks and how well management addresses those risks. A company in a high-risk sector like oil and gas can still receive a strong ESG score if its risk management is exceptional. That surprises many people, but it reflects the financial materiality focus of the methodology.

The practical challenge for ESG analysis techniques is that different rating providers prioritize different things. MSCI focuses on risk management. Sustainalytics emphasizes unmanaged risk. CDP focuses on disclosure quality. A company or fund can score very differently across providers without any underlying change in its actual ESG practices.

Pro Tip: Always ask what a rating is actually measuring before relying on it. A high MSCI ESG score means the company manages ESG-related financial risks well. It does not necessarily mean the company is a positive force for the environment or society. Understanding this distinction is critical for client communication and fund due diligence. You can also review frameworks for risk assessment to see how ESG risk fits into broader investment risk frameworks.

Sustainable investment performance: What the evidence really shows

Understanding measurement is vital, but how do sustainable strategies actually stack up against traditional investments in performance? Let’s look at what the research says, because the narrative is far more nuanced than either proponents or critics typically acknowledge.

The honest answer is that there is no single, universal performance result. Sustainable investing performance vs. conventional benchmarks is an empirical question with mixed findings; some evidence finds no statistically significant outperformance. Studies covering Eurozone ESG ETFs from 2019 to 2023 illustrate this well. During periods of market stress, such as the COVID-19 crash and early recovery, ESG-heavy portfolios often held up better due to lower exposure to energy and higher exposure to technology and healthcare. But during the 2022 energy crisis triggered by the Russia-Ukraine conflict, the same portfolios underperformed because they excluded many of the fossil fuel companies that surged in price.

The evidence does not support a blanket expectation of alpha from sustainable strategies. Performance is highly sensitive to market regime, benchmark selection, and the specific methodology used to construct the portfolio.

This is a critical insight for professionals. Clients and employers who expect sustainable funds to consistently outperform are working from a flawed premise. The more defensible case for sustainable investing rests on risk management, regulatory alignment, and long-term value creation, not short-term alpha generation.

Factors you must consider when evaluating sustainable fund performance:

-

Benchmark selection: ESG funds compared to a broad market index may look different than when compared to a sector-adjusted benchmark

-

Time period: Performance during market crises may not generalize to normal market conditions

-

Strategy type: ESG integration, thematic, and impact funds have different return profiles

-

Factor exposure: Many ESG funds are inadvertently tilted toward growth and quality factors, which drove strong performance in the 2010s but not in all regimes

-

Geographic concentration: European ESG funds often underweight energy-heavy markets, creating structural differences from global benchmarks

Understanding these nuances is what separates a credible sustainable finance professional from someone who simply repeats marketing claims. Risk rules in market cycles apply just as much to sustainable portfolios as to any other strategy.

What most guides miss: Why nuanced ESG analysis trumps labels

Most public discourse about sustainable investing focuses on two questions: Does it outperform? And is it real or just greenwashing? Both are valid, but they miss the deeper skill that separates good ESG analysts from great ones.

The real expertise lies in understanding the methodology and motivations behind each fund and rating. A fund label tells you almost nothing. An Article 8 fund under SFDR could be a sophisticated multi-factor ESG integration strategy or a basic exclusion screen with minimal analysis. Both carry the same regulatory label. The difference is buried in the fund’s methodology documentation, its principal adverse impact (PAI) statements, and its engagement policy.

Methodological differences in ESG/risk measurement can produce genuinely different investor conclusions. Rating and assessment approaches diverge in what they measure, whether that’s financial materiality, unmanaged risk, or disclosure quality. This means that a single ESG score, from any provider, is not a sufficient basis for investment decisions or client recommendations. You need to understand what the score is measuring, how it was constructed, and what it does not capture.

The blind spots are significant. Most ESG ratings rely heavily on disclosed data, which means companies with strong disclosure practices score well even if their actual environmental or social performance is mediocre. Smaller companies and those in emerging markets are often penalized simply for having less disclosure infrastructure, not for worse ESG performance. This creates systematic biases that sophisticated practitioners must account for.

The opportunity for finance professionals is real. As deep-dive ESG analysis courses make clear, the analysts who can look past the label, interrogate the methodology, and identify genuine value or risk are the ones who will stand out in this field. The market is still maturing. The professionals who invest in genuine methodological literacy now will have a significant edge as regulatory requirements tighten and client expectations grow.

Pro Tip: Always request the methodology documentation for any ESG rating or fund you’re evaluating. Ask specifically: What is this score measuring? What data sources does it rely on? What does it not capture? These questions reveal more about a fund’s genuine ESG credentials than any headline rating.

Take your expertise further with Verdant

To turn these insights into real-world results, high-quality education and up-to-date methodologies are essential. Understanding the difference between ESG integration, sustainable investment, and impact investing is just the starting point.

Verdant Institute offers structured learning tracks designed specifically for finance professionals and students who want to move beyond surface-level ESG knowledge. Whether you’re building foundational skills or working through advanced topics like transition finance and net-zero strategies, the platform’s library of 16 courses and over 160 lessons gives you the depth and rigor the industry demands. You can explore ESG investing courses across every major sustainable finance topic, track your CPD hours, and earn recognized certifications. Flexible plans make it accessible whether you’re a student at $18/month or a working professional at $58/month. Check Verdant pricing and learn more about Verdant Institute to find the right fit for your goals.

Frequently asked questions

How is sustainable investment different from responsible or ethical investing?

Sustainable investment specifically requires measurable environmental or social benefits and processes that avoid harm, while responsible or ethical investing may simply screen for certain values. Under SFDR’s definition, sustainable investment carries a documented evidence requirement that ethical investing does not.

What is the main regulatory standard for sustainable investment in Europe?

The SFDR defines and governs sustainable investment for regulated funds, including Article 9 funds in the EU. It requires that sustainable investment generate clear measurable social and/or environmental benefits without doing significant harm to other objectives.

How do providers calculate an ESG fund rating?

Fund-level ESG ratings, like MSCI’s methodology, aggregate and rescale the ESG scores of each holding based on their fund weighting, then adjust for data coverage to produce a final score.

Why do ESG ratings for the same fund sometimes differ between providers?

Differences in methodology, including what is measured, how data is weighted, and what data sources are used, lead rating agencies to diverge in their conclusions even when evaluating the same fund or company.