ESG is no longer a policy statement that lives in a responsible investment framework document. The role of ESG in asset allocation has shifted from signaling intent to driving concrete portfolio construction decisions, with measurable sustainability outcomes sitting alongside traditional return targets. Finance professionals who treat ESG as a compliance overlay miss what is actually happening at the portfolio level: allocation decisions are being shaped by ESG data, model choices, stewardship mandates, and asset-class constraints that carry direct implications for risk-adjusted returns. This article cuts through the generic framing and focuses on how ESG integration actually operates across strategic frameworks, quantitative models, and specific asset classes.

Key Takeaways

| Point | Details |

|---|---|

| ESG is operational, not decorative | Over 81% of PRI signatories now identify specific sustainability outcomes, moving well beyond policy statements. |

| Model choice changes everything | Linear ESG penalties concentrate portfolios; nonlinear methods preserve diversification while achieving meaningful ESG tilts. |

| Asset class constraints matter | LDI, fixed income, and equities each require distinct ESG integration techniques due to structural differences. |

| Governance is enforcing ESG goals | ESG-related contract clauses with external managers grew 10 percentage points since 2024, reflecting real accountability. |

| Quantitative skills are now required | Scenario analysis, forward-looking analytics, and sustainability metrics are integral to professional ESG practice today. |

The role of ESG in asset allocation frameworks

Sustainable asset allocation, as the industry now calls integrated ESG-aware portfolio construction, operates at two levels. At the strategic level, ESG factors inform long-horizon capital market assumptions, asset class expected returns, and risk parameters. At the tactical level, ESG data and ratings adjustments influence how allocators tilt within asset classes, exclude certain exposures, or weight toward sustainability outcomes.

The shift from ESG policy to practice is now well documented. With 81% of PRI signatories identifying specific sustainability outcomes and 70% acting on them, you can see that ESG factors in investing have migrated from aspirational language to hard portfolio objectives. That matters for asset allocation committees, because sustainability targets now compete directly with return and volatility constraints in the optimization process.

The fiduciary rationale for ESG inclusion has also matured. Modern investment mandates typically include:

- Climate transition risk in capital market assumptions for long-horizon portfolios

- Biodiversity and nature-related financial risks as systemic considerations in diversification

- Social factors, particularly labor practices and supply chain exposure, as earnings quality signals

- Governance quality metrics as leading indicators of management risk in equity sleeves

Pro Tip: When drafting investment policy statements, avoid vague ESG language like "integrate where possible." Specify which ESG outcome metrics the allocation framework will track and how they interact with return targets. Ambiguity creates accountability gaps that are difficult to close at the monitoring stage.

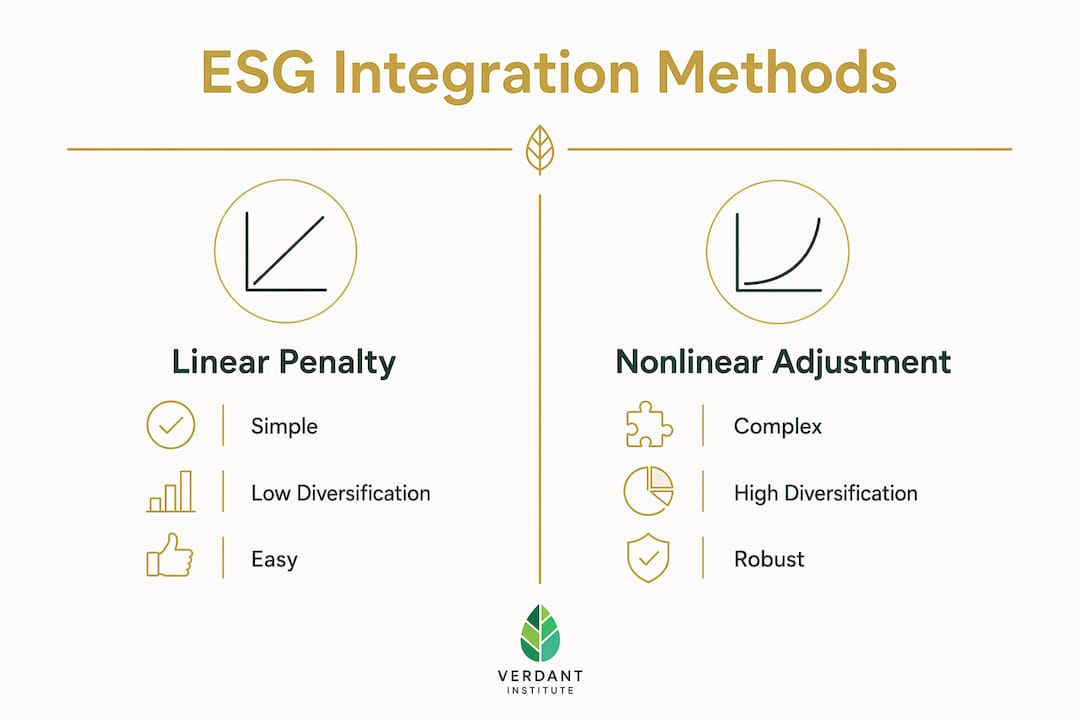

How modeling choices affect ESG portfolio outcomes

This is where most practitioners get surprised. The mathematical approach you use to incorporate ESG considerations into a mean-variance optimization determines portfolio concentration and diversification just as much as the ESG data itself.

The most common approach applies a linear penalty to assets with lower ESG scores, effectively reducing their expected return in the optimizer. The problem is predictable: the optimizer responds by concentrating holdings in a narrow set of high-scoring assets. Linear ESG penalties concentrate asset weights, reducing diversification in ways that can undermine the risk management objectives the allocation was designed to serve.

A more technically sound method uses nonlinear, ambiguity-based ESG adjustments rooted in robust mean-variance frameworks. This approach treats ESG uncertainty as a form of parameter ambiguity, adjusting portfolio weights in a way that captures the ESG tilt without forcing the optimizer into corner solutions.

| Integration method | ESG tilt achieved | Diversification impact | Implementation complexity |

|---|---|---|---|

| Linear penalty | High | Significant reduction | Low |

| Exclusion screens | Moderate | Moderate reduction | Low to medium |

| Tilting and reweighting | Moderate to high | Minimal if calibrated | Medium |

| Nonlinear ambiguity-based | High | Preserved | High |

Empirical findings from 2026 confirm that nonlinear methods achieve meaningful ESG improvements while keeping portfolios diversified and stable. For asset allocation committees, this means the conversation about ESG integration must include the quantitative team. Model validation should explicitly test how different ESG integration methods affect tracking error, concentration metrics, and Sharpe ratios before implementation.

Pro Tip: Request side-by-side optimization outputs from your quant team using both linear and nonlinear ESG integration approaches. The concentration difference in the resulting portfolios will make the tradeoffs concrete and anchor the governance discussion around evidence rather than preference.

ESG integration by asset class

The role of ESG in equity valuation, credit analysis, and liability-driven investing differs substantially, and treating them uniformly is one of the most common errors in practice. Here is how integration actually works across the main asset classes.

Equities

Equity portfolios have the widest ESG toolkit available. ESG scoring, active stewardship, engagement programs, exclusion lists, and best-in-class tilts can all be deployed. The role of ESG ratings agencies matters here: scores from providers like MSCI, Sustainalytics, and others feed directly into screening and weighting decisions. You should always understand what an ESG score is measuring before you use it, since ESG ratings agencies disagree with each other at rates that would surprise most allocators. This divergence is itself a risk that needs to be modeled, not ignored.

Engagement and stewardship in equities allow asset owners to influence corporate behavior rather than simply screen it out. A company with poor current scores but credible improvement trajectory may represent more value than a static high scorer, which is why forward-looking analysis is gaining ground alongside point-in-time ratings.

Fixed income and credit

The role of ESG in credit analysis is increasingly forward-looking rather than backward-looking. Historical ESG scores tell you what a borrower did. What credit portfolio managers need to know is whether the issuer has a credible transition plan, and how climate and biodiversity risks affect future cash flows and default probability.

Forward-looking climate and biodiversity analytics allow credit managers to identify which issuers are genuine transition leaders versus those managing optics. Labelled bonds, including green, social, and sustainability-linked bonds, provide another integration mechanism, offering use-of-proceeds transparency that generic bond investing cannot deliver. You can learn more about how this works in practice through ESG fixed income integration.

Liability-driven investments

LDI is the hardest case. The hedging instruments central to LDI strategies, including sovereign bonds, interest rate swaps, and repos, carry counterparty and sovereign issuer constraints that limit direct ESG integration. Full ESG integration is difficult in these instruments, and practitioners who force it without accounting for these constraints create operational and liquidity risks.

The workable approach combines partial ESG solutions:

- Exclusion lists for the most problematic sovereign or corporate issuers where liquidity allows

- Labelled bond incorporation in the credit overlay or return-seeking sleeve

- Stewardship activity directed at the managers running LDI mandates

- Climate scenario analysis to stress-test duration matching under transition risk conditions

Tailored ESG approaches in LDI require reconciling sustainability goals with hedging requirements, and that reconciliation must happen at the mandate design stage, not after the fact.

Governance, stewardship, and manager oversight

Governance is the mechanism that translates ESG goals into portfolio reality. Without it, even the most carefully designed ESG allocation framework degrades into a reporting exercise.

Asset owners exercise tighter RI oversight than their managers, applying Paris Agreement frameworks more extensively and enforcing climate scenario analysis at the manager selection stage. This asymmetry matters because it means institutional clients are often ahead of their managers on ESG implementation standards.

The governance infrastructure that makes ESG-driven allocation work includes:

- Board-level sustainability outcome metrics that connect portfolio decisions to measurable real-world targets, not just portfolio-level scores

- Stewardship KPIs embedded in manager reporting requirements, covering voting records, engagement outcomes, and escalation procedures

- Contractual ESG clauses with external managers: ESG-related contract clauses grew by 10 percentage points since 2024, reflecting an enforcement trend that is accelerating

- Regular scenario analysis reviews that incorporate both physical and transition climate risks at the total portfolio level

The role of CFA professionals in ESG is increasingly linked to this governance layer. CFA charterholders working in asset allocation or manager research are expected to understand how ESG mandates interact with fiduciary obligations, and the CFA Institute's published guidance explicitly connects ESG integration to the duty of loyalty and prudent investor standards. Getting this governance structure right is what separates portfolios with genuine ESG integration from those with strong messaging and weak implementation.

Pro Tip: Include ESG reporting requirements in manager contracts at the mandate design stage, specifying the exact metrics, frequency, and escalation procedures. Adding them later as amendments is possible, but you lose negotiating leverage and create gaps in historical data that complicate performance attribution.

Implementing ESG in institutional portfolios

Translating the frameworks above into operational practice requires a structured approach across several dimensions. The following practices reflect what well-implemented ESG-integrated allocations actually do.

- Assess sustainability outcomes explicitly alongside financial targets in the investment policy statement, with defined metrics that connect to the UN SDGs or Paris Agreement where the mandate supports it

- Use multiple ESG data sources rather than relying on a single ratings provider, acknowledging divergence and building it into your sensitivity analysis

- Run climate scenario analysis across the entire portfolio, not just the equity sleeve, to identify aggregate transition risk and physical risk concentrations

- Design ESG tilts with explicit diversification budgets: set a maximum acceptable tracking error from the ESG integration and validate that the optimization method used stays within it

- Review ESG portfolio construction approaches periodically as data quality, regulatory requirements, and analytical tools evolve

- Avoid treating ESG integration as a one-time exercise. Markets, issuer practices, ratings methodologies, and regulatory standards all change. Build in annual reviews of the ESG framework itself, not just the underlying positions

The most common pitfall is implementing ESG at the asset manager level without aligning it with the total portfolio objectives set at the asset owner level. Misalignment between manager-level ESG scoring and portfolio-level sustainability outcomes creates attribution problems and makes it nearly impossible to answer the question: did we actually achieve what we set out to do?

My take on what most practitioners are still missing

I've worked with enough allocators to know that the conversation about ESG integration often stalls at the wrong level. Teams spend months debating which ESG ratings agency to use or whether to exclude a particular sector, and relatively little time examining whether their modeling choices are undermining their own diversification goals.

What I've found is that the model is the message. If you implement ESG using a linear penalty and then wonder why your portfolio looks concentrated, the answer isn't your data. It's your methodology. Most asset allocation teams have not validated their ESG integration approach quantitatively, and that gap shows up in ways that are easy to misattribute to "ESG constraints" rather than model design.

I'm also skeptical of the tendency to treat governance as a downstream reporting function. The most effective ESG-integrated allocations I've seen build governance into the mandate design from day one. That means stewardship KPIs in contracts before the first dollar is invested, not attached afterward as an afterthought.

The next frontier, and one where current practice still falls short, is granular forward-looking analytics by asset class. Backward-looking ESG scores are losing credibility with sophisticated allocators, particularly in credit and LDI. The teams investing in climate scenario modeling and biodiversity impact analysis at the issuer level today are building a genuine informational advantage.

— Charles

Build your ESG asset allocation expertise with Verdant Institute

If this article clarified where ESG integration really lives in the investment process, the next step is deepening those skills with structured learning. Verdant Institute offers a full e-learning ecosystem built specifically for finance professionals working in sustainable finance and ESG analysis. Courses cover everything from ESG portfolio construction fundamentals to advanced topics including transition finance and net-zero strategies, with over 160 lessons across 16 structured courses.

Whether you are building your first ESG-integrated mandate or stress-testing an existing framework, Verdant's professional learning tracks give you the technical grounding to make implementation decisions with confidence. CPD tracking and certifications are included, making it practical for institutional practitioners managing development requirements. Plans start at $58 per month for professionals, with student pricing available at $18 per month.

FAQ

What is the role of ESG in asset allocation?

ESG factors influence asset allocation by shaping capital market assumptions, exclusion criteria, portfolio tilts, and sustainability outcome targets. Modern allocators integrate ESG at both the strategic and tactical levels, treating it as a material input into risk-adjusted return analysis.

How does ESG integration differ across asset classes?

Equities support the widest range of ESG techniques including scoring, engagement, and exclusions. Fixed income relies on forward-looking transition analytics and labelled bonds. LDI faces structural hedging constraints that limit direct ESG integration, requiring a hybrid approach combining exclusions, labelled bonds, and stewardship.

Why do linear ESG penalties cause concentration problems?

A linear penalty reduces expected returns for low-scoring assets, which pushes the optimizer toward a narrow set of high-scoring names. Nonlinear ambiguity-based methods treat ESG uncertainty more realistically, achieving equivalent tilts while preserving diversification.

What is the role of ESG in credit analysis?

In credit, ESG integration is most effective when it uses forward-looking climate and nature analytics to assess issuer transition credibility rather than relying only on historical ESG scores, which reflect past behavior rather than future default risk.

How are asset owners enforcing ESG mandates with external managers?

Asset owners are embedding ESG clauses in manager contracts, requiring climate scenario analysis, and tracking stewardship KPIs. ESG-related contractual requirements with external managers grew 10 percentage points between 2024 and 2026, reflecting a clear enforcement trend.