Fixed income professionals are increasingly expected to do something equity analysts figured out earlier: embed ESG factors into the core of their credit analysis. Yet ESG in fixed income explained properly remains rare, even in professional circles. The mechanics differ substantially from equities. Bond investors don't benefit from upside; they need to focus on not losing. That asymmetry changes everything about how ESG criteria for fixed income should be applied, weighted, and acted upon. This article cuts through the noise and gives you a framework built for credit markets, not the stock market.

Table of Contents

- Key Takeaways

- ESG in fixed income explained: what the fundamentals actually mean

- Market size, regulations, and the data quality problem

- How ESG integration affects portfolio performance and credit spreads

- Practical integration: how to actually do it

- Emerging trends shaping the future of ESG fixed income

- My honest take on where ESG integration in fixed income falls short

- Take your ESG knowledge to the next level with Verdantinstitute

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| ESG differs from equities | Fixed income focuses on downside protection, making ESG a risk anticipation tool rather than a growth signal. |

| Integration beats screening | Embedding ESG metrics into credit analysis surfaces material risks that negative screening consistently misses. |

| Data divergence is real | ESG rating agencies show an average correlation of 0.54, versus 0.99 for credit ratings, requiring multi-source triangulation. |

| Regulation is reshaping disclosure | EU CSRD, ISSB standards, and SFDR frameworks are raising the floor for material ESG disclosure in bond markets. |

| Greenium has measurable pricing impact | Investors accept slightly lower yields on climate bonds, reflecting net-zero alignment and long-term risk reduction. |

ESG in fixed income explained: what the fundamentals actually mean

ESG stands for Environmental, Social, and Governance. You already know that. What matters here is understanding how each pillar maps to credit risk rather than shareholder value.

Environmental factors cover climate exposure, carbon transition costs, physical asset risk, and regulatory penalties tied to emissions. Social factors include labor relations, supply chain standards, community impact, and product liability. Governance factors address board independence, executive accountability, audit quality, and capital allocation discipline. In fixed income, all three act as early warning signals for credit deterioration, not just reputational noise.

The key distinction between fixed income and equity ESG investing is the directionality of risk exposure. Fixed income investors focus on downside protection and credit distress indicators, not growth potential. An equity investor can tolerate a governance red flag if the growth story is compelling enough. A bondholder cannot. Default risk is binary. That asymmetry demands more rigorous ESG scrutiny upfront.

Two primary approaches exist for ESG factors in bond markets:

- ESG integration: Incorporates material ESG data directly into credit spreads, issuer assessments, and portfolio construction. It doesn't exclude issuers automatically; it adjusts the risk premium.

- ESG screening: Excludes certain issuers or sectors based on predefined ESG criteria. Negative screening removes tobacco, coal, or weapons. Positive screening tilts toward best-in-class performers.

ESG integration surfaces overlooked financial risks that traditional credit analysis misses. A coal utility rated investment grade by legacy metrics may carry significant stranded asset risk that only an ESG-integrated lens would flag before spread widening occurs.

Pro Tip: Don't treat ESG integration and screening as either/or choices. The most effective sustainable fixed income strategies use integration as the foundation and apply targeted screening for specific mandate constraints.

Market size, regulations, and the data quality problem

The market for sustainable fixed income is no longer a niche. The global climate bond market reached $6.8 trillion in cumulative volume by Q2 2026, with over $1 trillion in annual issuance for three consecutive years and more than 400 new issuers entering the market in 2025 alone. The sustainable fixed income market has moved from an ethical preference to a structural feature of global bond markets.

Regulatory frameworks are now hardwiring ESG disclosure into standard reporting. Here is a snapshot of the regulations you need to track:

| Regulation | Jurisdiction | Core Requirement |

|---|---|---|

| EU CSRD | European Union | Double materiality reporting; mandatory sustainability statements |

| ISSB IFRS S1/S2 | Global | Climate and general sustainability disclosure standards |

| SFDR Articles 6/8/9 | European Union | Fund-level ESG classification and product disclosure |

| SEC Climate Disclosure Rule | United States | Material climate risk disclosure for public companies |

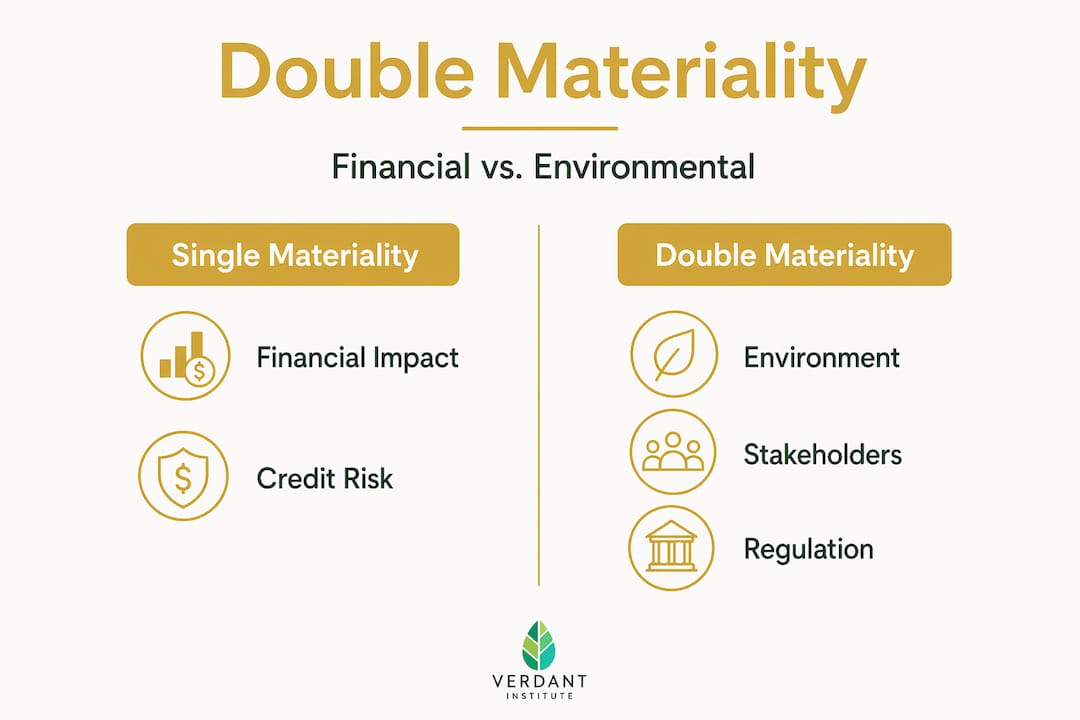

These frameworks are converging toward a concept you need to understand precisely: double materiality. Single materiality asks how ESG factors affect the issuer's financial performance. Double materiality adds the reverse question: how does the issuer affect the environment and society? The EU CSRD mandates the dual materiality lens, and that is reshaping what bond investors can demand in disclosure documents.

The data quality problem is real and persistent. ESG ratings agencies show an average correlation of just 0.54 between their ratings, compared to 0.99 for traditional credit ratings. That divergence creates practical challenges. An issuer rated AA by one ESG provider might be rated BB by another, based on different methodologies, weightings, and data sources. Relying on a single ESG score in your credit process is not analysis. It's delegation.

The push toward decision-useful sustainability disclosure is gaining urgency precisely because of this divergence. Investors are demanding standardized, audited, issuer-reported data that reduces their dependence on third-party intermediaries with inconsistent methodologies.

How ESG integration affects portfolio performance and credit spreads

The evidence linking ESG integration to financial performance has grown more credible. A NYU Stern 2025 meta-analysis of 1,400 studies found that 58% show a positive correlation between ESG integration and financial performance, with only 13% showing negative correlation. The weight of evidence now favors integration, though the effect size and channels vary by sector, region, and asset class.

In fixed income specifically, climate transition risk is where the performance link is clearest. A PIMCO 2025 study found that incorporating climate transition risk into credit spread assessments reduced portfolio drawdowns by 18% during 2024 energy market volatility. That is a material risk reduction figure, not a marginal one.

The greenium concept is increasingly relevant for fixed income portfolio managers. Investors accept slightly lower yields on climate bonds because of their alignment with net-zero commitments and portfolio risk management goals. The greenium reflects both demand-side pressure from ESG-mandated funds and supply-side credibility signals from rigorous green bond frameworks. It is not charity. It is rational pricing behavior in a market where climate risk is increasingly repriced.

Sovereign bonds add another layer of complexity. Stronger governance and economic readiness are linked to lower sovereign borrowing costs, with credible climate governance reducing yields by approximately 2 basis points per 10-point improvement in climate governance indices. Importantly, sovereign bond markets price credible governance and green infrastructure delivery, not ambition statements alone. Investors are learning to distinguish policy credibility from policy theater in their ESG portfolio construction frameworks.

Social factors, by contrast, show a more mixed relationship with credit pricing. In some cases, labor disputes or supply chain controversies have widened spreads temporarily but reverted quickly. The materiality of social factors depends heavily on sector, jurisdiction, and the duration of the bond in question.

Practical integration: how to actually do it

Understanding ESG in investments conceptually is necessary. Applying it systematically in a fixed income workflow is where most professionals get stuck. Here is a structured approach:

-

Distinguish green bond standards before you buy. Process-based standards provide flexible frameworks that issuers self-certify against. Science-based standards require third-party verification and alignment with quantified emissions pathways. Institutional fixed income investors increasingly require the latter. Know which you are holding.

-

Embed ESG metrics into your credit risk framework. ESG metrics must be integrated into enterprise risk management at the issuer level, linking ESG key risk indicators with financial KPIs. Ask whether the issuer you are analyzing has done this internally. If ESG data sits outside their risk governance structure, that itself is a governance flag.

-

Triangulate across at least three ESG data sources. Given the 0.54 average correlation between ESG rating providers, using a single source creates a false sense of precision. Build an internal scoring framework that weights provider data alongside your own qualitative assessment of management quality, disclosure transparency, and regulatory exposure.

-

Apply the dual materiality lens systematically. Assess both how ESG factors affect the issuer's credit profile and how the issuer's operations affect the environment and communities. The sustainable investing frameworks that hold up longest are those built on both dimensions, not just financial materiality.

-

Set outcome-based targets, not just process targets. Committing to "consider ESG factors" is not a strategy. Define specific thresholds: minimum carbon disclosure scores, governance independence ratios, or maximum revenue exposure to high-transition-risk sectors.

Pro Tip: The most common error in sustainable fixed income strategies is confusing having an ESG policy with doing ESG analysis. A policy describes intent. Integration requires consistent, documented application of ESG criteria in every credit decision, backed by the data to prove it.

Emerging trends shaping the future of ESG fixed income

Several developments will define how ESG factors in bond markets evolve over the next three to five years.

Sustainability-linked bonds (SLBs) represent the fastest-growing segment, but also the most integrity-challenged. Unlike green bonds, SLBs tie coupon payments to the issuer meeting specific ESG performance targets. The problem: only 40% of SLBs met the Climate Bonds Initiative's alignment criteria in 2025. Target ambition levels, baseline definitions, and verification standards remain inconsistent across the market.

Sovereign ESG integration is maturing but unevenly. Macroeconomic credit assessment increasingly incorporates climate governance scores, transition readiness indicators, and physical risk exposure at the country level. Investors in sustainable investment markets are beginning to differentiate between sovereigns based on credible policy delivery rather than headline pledges.

Social impact measurement remains the least mature dimension. Environmental metrics have standardized pathways. Social factors, covering labor, health, equity, and community resilience, lack equivalent measurement frameworks. That gap is narrowing as ISSB and CSRD disclosure requirements begin generating comparable social data sets.

The investor expectation curve is also shifting. Beyond risk mitigation, fixed income investors are increasingly demanding proof of positive impact. Transparency, accountability, and outcome reporting are moving from nice-to-have to contractual obligation in many institutional mandates.

My honest take on where ESG integration in fixed income falls short

I've reviewed ESG integration frameworks across dozens of credit teams, and the pattern I keep seeing is the same. Analysts know ESG matters. They produce ESG assessments. Then those assessments sit in a separate report, disconnected from the credit recommendation memo where the actual decision gets made.

That structural disconnect is the real problem. ESG in fixed income doesn't fail because people don't care. It fails because the incentive structures, reporting lines, and decision workflows haven't been rebuilt to incorporate it. Credit committees still primarily respond to financial ratios. Until ESG key risk indicators are directly wired to the credit spread model, they remain advisory at best.

What I've found actually works is starting with governance. Governance factors are the most directly translatable to credit quality, the most consistently disclosed, and the most measurable in short-term bond timescales. Analysts who begin there build credibility internally before tackling harder environmental and social questions.

The regulatory wave from EU CSRD and ISSB is forcing the issue in a way that voluntary frameworks never could. For the first time, credit analysts are getting issuer-level sustainability data in audited, standardized form. That changes the analysis. Not overnight. But it's happening.

My advice: stop treating ESG as a compliance layer and start treating it as a leading indicator system. The analysts who do that will make better credit calls. That's the whole point.

— Charles

Take your ESG knowledge to the next level with Verdantinstitute

If you're applying ESG criteria in fixed income portfolios and want structured, practitioner-level training to back it up, Verdantinstitute was built for exactly that. The platform offers 16 courses and over 160 lessons spanning ESG fundamentals, transition finance, net-zero strategy, and advanced ESG topics tailored specifically for finance professionals. CPD tracking, certifications, and structured learning tracks mean you build verifiable expertise, not just general awareness. Plans start at $18 per month for students and $58 per month for professionals. Visit the Verdantinstitute pricing page to find the plan that fits your role and learning goals. Learning why ESG matters in bonds is the first step. Being able to apply it rigorously is what separates good credit analysts from great ones.

FAQ

What makes ESG in fixed income different from equities?

Fixed income investors focus on downside protection and credit risk, not growth. ESG factors serve as early warning indicators for credit deterioration, making their application more risk-oriented than in equity analysis.

How do ESG factors affect bond yields and credit spreads?

Strong ESG profiles are linked to tighter credit spreads and lower borrowing costs. Climate transition risk embedded in credit models reduced portfolio drawdowns by 18% during 2024 volatility, according to a PIMCO 2025 study.

What is the greenium in climate bonds?

The greenium is the yield premium investors forgo when buying climate-aligned bonds. It reflects strong demand from ESG-mandated institutional buyers and signals confidence in the issuer's net-zero alignment.

Why do ESG ratings diverge so much between providers?

ESG rating agencies use different methodologies, data sources, and materiality weightings, producing an average inter-provider correlation of just 0.54. That is why fixed income professionals should triangulate across multiple sources rather than relying on a single score.

How do I evaluate whether a green bond is credible?

Check whether the bond meets science-based standards with third-party verification, not just process-based self-certification. Only 40% of sustainability-linked bonds met Climate Bonds Initiative criteria in 2025, so framework rigor is a critical due diligence factor.