ESG screening methodology is the structured process of evaluating investments against environmental, social, and governance criteria to determine portfolio eligibility. Finance professionals use it to filter out harmful holdings, identify sustainability leaders, and manage long-term risk. Providers like Sustainalytics and data platforms like EcoVadis have built entire product lines around it. With 71% of global dealmakers reporting that ESG screening has grown significantly more important in due diligence over the past 12–18 months, understanding how this methodology works is no longer optional for serious investors.

What is ESG screening methodology and why does it matter?

ESG screening methodology is the formal system an investor or institution uses to assess whether a company, fund, or asset meets defined environmental, social, and governance standards before inclusion in a portfolio. The industry also refers to this process as ESG evaluation or sustainability screening. These terms are used interchangeably in practice, but the underlying logic is the same: apply a consistent, repeatable framework to separate qualifying investments from those that fail your criteria.

The methodology matters because it converts abstract sustainability values into concrete investment decisions. Without a defined process, ESG claims are just marketing. With one, you can document why a holding was included or excluded, defend that decision to regulators, and update it as new data arrives. The ESG criteria selection process should begin with a formal materiality assessment tailored to the specific industry, not a blanket checklist applied uniformly across sectors.

Materiality is the key word here. A carbon emissions threshold matters far more for an energy company than a software firm. Water usage is financially relevant for agriculture but largely irrelevant for a consulting business. Screening criteria that ignore industry context produce noisy, unreliable results.

What are the main types of ESG screening approaches?

Three core screening approaches define the field. Each serves a different investment purpose, and most sophisticated portfolios combine more than one.

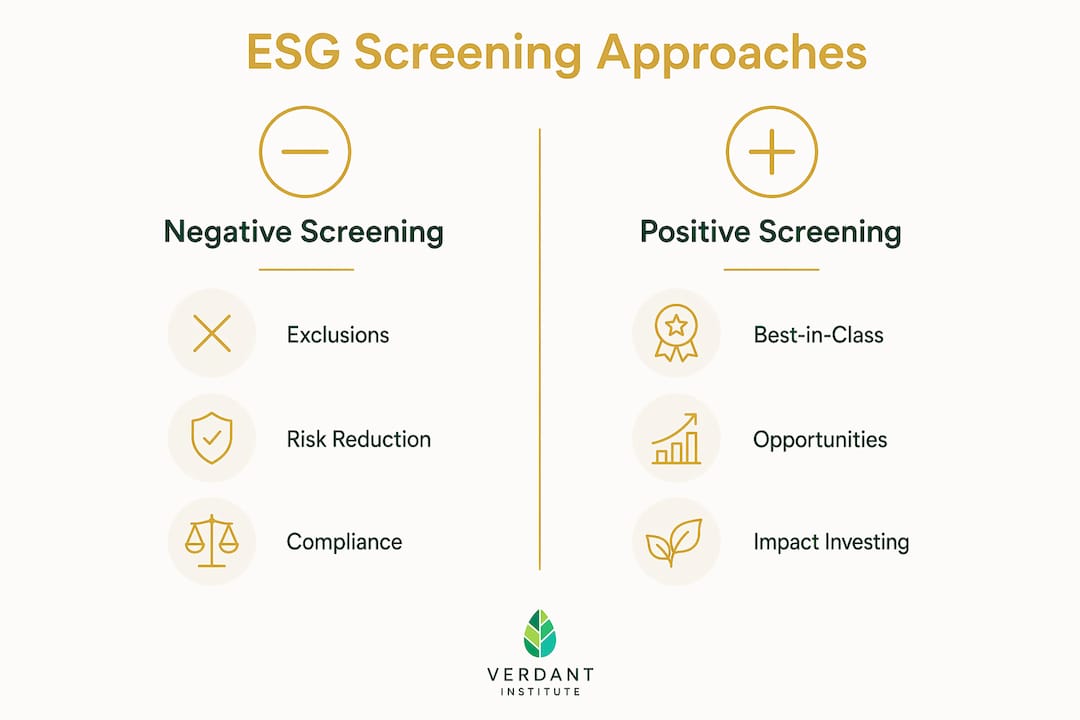

Negative screening (also called exclusionary screening) removes companies or sectors that fail to meet minimum standards. Common exclusions include tobacco manufacturers, weapons producers, fossil fuel extractors, and companies with serious human rights violations. This is the oldest and most widely used form of ESG screening. It is straightforward to implement and easy to communicate to clients.

Positive screening, often called best-in-class screening, takes the opposite approach. Instead of excluding the worst actors, it actively selects the top ESG performers within each sector. A positive screen might include the top 20% of energy companies by ESG score, even if those companies still produce oil. The logic is that rewarding leaders creates market incentives for improvement across the industry.

Norms-based screening evaluates companies against international standards rather than investor-defined thresholds. The most common reference frameworks include:

- The UN Global Compact principles on human rights, labor, environment, and anti-corruption

- The OECD Guidelines for Multinational Enterprises

- The ILO core labor standards

Sustainalytics, for example, scans over 700,000 news items daily from 60,000 global media and NGO sources to detect breaches of these international norms. That scale of monitoring is what makes norms-based screening dynamic rather than static.

Pro Tip: Combining negative and norms-based screening gives you a floor (no excluded sectors) and a ceiling (ongoing compliance with global standards). Adding a positive screen on top creates a portfolio that avoids the worst, monitors for breaches, and rewards the best.

How is ESG screening implemented in practice?

Implementing an ESG screening process involves four operational steps: criteria selection, data gathering, scoring or rating, and ongoing monitoring. Each step has distinct tools and common failure points.

Criteria selection and materiality

Materiality assessment ensures your screening criteria reflect financially relevant sustainability factors for the specific industry you are analyzing. A useful starting point is the SASB (Sustainability Accounting Standards Board) materiality map, which identifies the ESG issues most likely to affect financial performance by sector. From there, you define specific thresholds: a revenue cutoff for tobacco exposure, a minimum governance score for board independence, or a maximum carbon intensity for climate-aligned portfolios.

Data sources for ESG screening

No single data source is sufficient. Effective ESG screening draws from multiple inputs simultaneously.

| Data Type | Source Examples | Primary Use |

|---|---|---|

| Corporate disclosures | Annual reports, sustainability reports, CDP filings | Baseline ESG performance data |

| Third-party ratings | Sustainalytics, MSCI ESG Ratings, ISS ESG | Peer comparison and scoring |

| Media and NGO monitoring | News feeds, NGO reports, regulatory filings | Real-time breach detection |

| Government and regulatory data | SEC filings, EU taxonomy disclosures | Compliance verification |

The combination of corporate disclosures and independent monitoring is critical. Relying solely on self-reported data risks greenwashing, since companies control their own narratives. External media and NGO monitoring catches what corporate reports omit.

Scoring systems and rating models

ESG ratings and ESG scores serve different functions. Numerical scores, typically on a 0–100 scale, integrate directly into quantitative portfolio models and allow for weighted comparisons across holdings. Categorical ratings, such as AAA through CCC used by MSCI, provide quick peer comparisons and are easier to communicate to non-technical stakeholders. Understanding what is ESG score meaning in context matters: a score of 72 means nothing without knowing the peer group, the weighting methodology, and the data vintage.

Pro Tip: When building a scoring model, weight ESG criteria by their SASB materiality ranking for the relevant sector. This prevents a high governance score from masking a critical environmental failure in an industry where environmental risk is the primary financial driver.

What are the common pitfalls in ESG screening?

ESG screening methodology breaks down in predictable ways. Knowing the failure modes in advance lets you build defenses into your process from the start.

"The most dangerous assumption in ESG screening is that a clean parent company means a clean portfolio. Subsidiary structures routinely hide the exposures that matter most." — PRI ESG Screening Primer

Greenwashing risk is the most widely discussed problem. Companies publish sustainability reports that emphasize positive initiatives while omitting material failures. The defense is straightforward: supplement corporate disclosures with independent monitoring from sources like NGO databases and regulatory filings.

Subsidiary creep is less discussed but equally damaging. Subsidiary creep occurs when a parent company passes your screens but its subsidiaries engage in excluded activities. A holding company might have no direct tobacco revenue while owning a subsidiary that manufactures cigarette filters. Entity-level analysis, not just parent-level review, is the only reliable solution.

The following pitfalls deserve explicit attention in any screening framework:

- Rating inconsistency: Different ESG rating agencies can assign vastly different scores to the same company. This is not a minor variance. Studies have documented correlation coefficients as low as 0.4 between major providers. Build an internal adjustment layer rather than accepting any single provider's output as definitive.

- Threshold ambiguity: Vague criteria like "limited fossil fuel exposure" create audit risk. Clear documentation of revenue cutoffs and specific thresholds is best practice for defensible, audit-ready methodologies.

- Static screening: ESG profiles change. A company that passed your screen two years ago may have since acquired a coal asset or faced a governance scandal. Continuous monitoring is not optional.

What are the benefits of ESG screening in portfolio management?

ESG screening produces measurable improvements in risk management, regulatory compliance, and client alignment. These are not soft benefits. They show up in portfolio performance and institutional credibility.

78% of investors report that structured sustainability metrics improve their confidence in assessing long-term corporate risk. That confidence translates into more defensible investment decisions and fewer surprise write-downs from ESG-related events. Companies with poor labor practices face regulatory fines. Those with weak governance face fraud risk. Screening for these factors before they become headlines is the point.

Reputational risk mitigation is a second concrete benefit. Holding a company that later appears in headlines for environmental violations or human rights abuses creates client relations problems that are expensive to manage. A documented screening process demonstrates due diligence and provides a defensible record if questions arise.

Regulatory alignment is a third driver. The EU's Sustainable Finance Disclosure Regulation (SFDR) and the SEC's climate disclosure rules both require asset managers to demonstrate how sustainability factors are integrated into investment processes. ESG screening methodology provides the documented framework that satisfies these requirements. The sustainable investment market continues to grow, and regulatory pressure is accelerating that trend.

How does ESG screening integrate with broader investment strategies?

ESG screening is one tool in a larger toolkit. Integrating it with other approaches produces more complete portfolios and stronger sustainability outcomes.

- Combine screening with ESG integration. Screening sets the eligibility universe. ESG integration then weights holdings within that universe based on ESG scores, adding a quantitative layer to the qualitative filter. Explore the full range of ESG investment strategies to understand where screening fits within the broader framework.

- Connect screening to engagement. When a holding approaches your exclusion threshold, active engagement with management can drive improvement rather than forcing divestment. This is particularly relevant for norms-based screening, where a breach may be remediable.

- Use scores for portfolio construction. Numerical ESG scores feed directly into ESG portfolio construction models, enabling optimization against both financial and sustainability objectives simultaneously.

- Schedule periodic reviews. ESG frameworks evolve. The EU Taxonomy, TCFD recommendations, and ISSB standards all update regularly. Build a quarterly review cycle into your screening process to realign criteria with current regulatory and market expectations. Regular portfolio reviews also catch data drift before it creates compliance gaps.

- Embed screening in compliance workflows. Integrating ESG screening with existing AML, KYC, and sanctions compliance systems creates a unified risk management framework. This reduces duplication and ensures ESG flags surface through the same channels as other risk alerts.

Key takeaways

Effective ESG screening methodology requires industry-specific criteria, multi-source data, and continuous monitoring to produce defensible, audit-ready investment decisions.

| Point | Details |

|---|---|

| Start with materiality | Tailor screening criteria to each industry's financially relevant ESG factors, not a generic checklist. |

| Use multiple data sources | Combine corporate disclosures with independent media and NGO monitoring to reduce greenwashing risk. |

| Distinguish scores from ratings | Numerical scores suit quantitative models; categorical ratings work better for peer comparisons and client reporting. |

| Screen at the entity level | Analyze subsidiaries, not just parent companies, to avoid inadvertent exposures through subsidiary creep. |

| Document every threshold | Clear revenue cutoffs and criteria definitions protect against audit risk and client misinterpretation. |

Where most ESG screening frameworks fall short

I have reviewed a lot of ESG screening frameworks across asset managers, development finance institutions, and corporate treasury teams. The most common failure is not a lack of data. It is a lack of judgment about which data matters.

Teams spend months selecting rating providers and building scoring models, then apply the same criteria to a pharmaceutical company and a mining company. The result is a framework that looks rigorous on paper but produces misleading outputs in practice. Materiality is not a compliance checkbox. It is the analytical core of the entire methodology.

The second pattern I see repeatedly is over-reliance on a single third-party rating provider. When Sustainalytics and MSCI disagree on a company by 30 points, that disagreement is information. It tells you the company's ESG profile is contested and warrants deeper analysis. Treating one provider's output as ground truth means you are outsourcing your judgment to a black box.

The practitioners I respect most build an internal view first, then use third-party ratings as a cross-check rather than a starting point. That approach takes more time upfront. It produces far more defensible decisions over the long run. If you want to build that kind of analytical depth, embedding ESG in investment decisions requires more than a subscription to a data provider. It requires a trained team that understands what the numbers actually measure.

— Charles

Build your ESG screening skills with Verdantinstitute

Understanding ESG screening methodology at a conceptual level is the starting point. Applying it to real portfolios, navigating data inconsistencies, and building audit-ready frameworks requires structured training.

Verdantinstitute offers dedicated learning tracks for both students and working professionals, covering ESG criteria selection, scoring systems, and portfolio integration from the ground up. The platform's Deep Dive courses go beyond definitions to cover materiality assessment, rating agency methodology, and practical screening implementation. Students access the full library for $18/month. Professionals get CPD-tracked certifications for $58/month. If you are serious about integrating sustainability into your investment process, explore Verdantinstitute's course offerings and review the pricing options that fit your role.

FAQ

What is ESG screening methodology in simple terms?

ESG screening methodology is the structured process of evaluating investments against environmental, social, and governance criteria to determine whether they qualify for inclusion in a portfolio. It combines criteria selection, data gathering, scoring, and ongoing monitoring into a repeatable framework.

How do negative and positive ESG screening differ?

Negative screening excludes companies that fail minimum ESG standards, such as tobacco or weapons manufacturers. Positive screening selects the top ESG performers within each sector, rewarding leaders rather than simply removing laggards.

What does an ESG score mean for investors?

An ESG score is a numerical measure, typically on a 0–100 scale, that quantifies a company's environmental, social, and governance performance. Scores enable quantitative portfolio modeling, while categorical ratings like AAA or CCC are better suited for peer comparisons.

Why do ESG ratings differ across providers?

Different rating agencies use different data sources, weighting methodologies, and materiality frameworks, producing significantly divergent scores for the same company. Investors should treat disagreements between providers as a signal for deeper analysis rather than defaulting to one source.

What is subsidiary creep in ESG screening?

Subsidiary creep occurs when a parent company passes ESG screens but its subsidiaries engage in excluded activities. Entity-level analysis of the full corporate structure is required to prevent inadvertent portfolio exposures.