An ESG audit is the structured evaluation of a company's environmental, social, and governance disclosures for accuracy, completeness, and compliance with recognized reporting standards. The esg audit process explained in this guide covers five sequential phases: defining materiality and scope, assessing data systems, gathering evidence, performing substantive testing, and issuing the final assurance report. Frameworks including GRI, SASB, TCFD, and CSRD each shape what gets audited and how. For finance professionals, understanding this process is no longer optional. Regulators, institutional investors, and lenders now treat ESG assurance as a baseline expectation for credible sustainability reporting.

What are the five core phases of the ESG audit process?

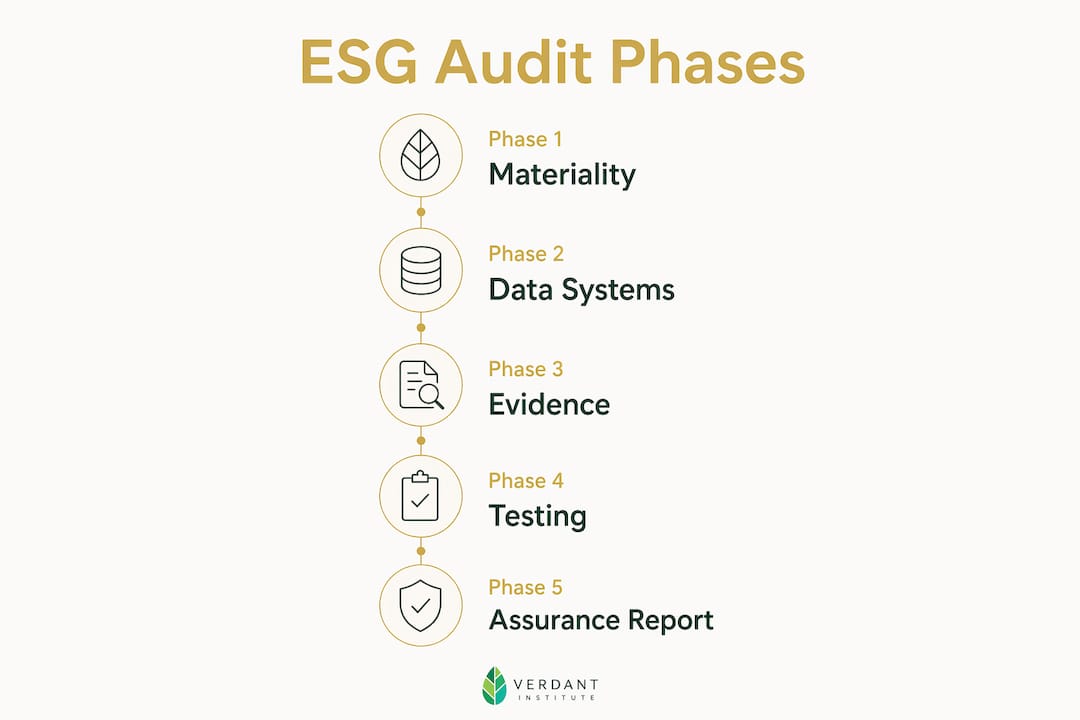

The five core phases of an ESG audit follow a logical sequence that mirrors financial audit methodology. Each phase builds on the previous one, and skipping any step creates gaps that auditors will flag.

Phase 1: Defining materiality and audit scope

Materiality determines which ESG topics are significant enough to require verification. Auditors and management align on the chosen reporting framework, whether GRI, SASB, TCFD, or CSRD, and identify which disclosures fall within scope. This scoping decision directly controls audit cost, timeline, and depth.

Phase 2: Assessing data collection systems

Auditors evaluate the tools, processes, and internal controls your organization uses to collect ESG data. They look for documented responsibilities, data validation steps, and system access logs. Weak controls at this phase signal higher risk and trigger more intensive testing later.

Phase 3: Gathering evidence and interviewing personnel

Stakeholder interviews with sustainability managers, HR, operations, and legal teams verify how ESG governance works in practice. Interviews reveal what documentation says versus what actually happens on the ground. Finance professionals should prepare teams for these conversations well in advance.

Phase 4: Substantive testing

Auditors perform recalculations, cross-checks, and direct verification of reported metrics against source documents. A carbon emissions figure, for example, gets traced back to utility invoices and conversion factors. Any discrepancy between reported data and source evidence triggers a finding.

Phase 5: Issuing the assurance report

The final assurance report specifies the scope, standards applied, assurance level, and key findings. Common assurance standards include AA1000AS, ISAE 3000, and ISAE 3410. The report is typically published alongside the ESG disclosure.

Pro Tip: Start scoping conversations with your auditor at least three months before the audit begins. Late scoping forces rushed evidence collection and increases the risk of material findings.

How do ESG audit frameworks and standards shape the process?

The chosen reporting framework determines which metrics require assurance, what materiality means, and how deeply auditors must test. GRI focuses on impact materiality, asking how the company affects people and the environment. SASB narrows scope to industry-specific financial materiality. TCFD centers on climate-related financial risk disclosures.

CSRD introduces the most demanding requirement: double materiality. Under this approach, auditors examine both how environmental and social factors affect the company financially and how the company's activities affect the world. That dual lens expands audit scope considerably compared to single-materiality frameworks.

Assurance levels also vary by framework and jurisdiction. Limited assurance under CSRD is the current default. It provides a moderate level of confidence by checking for material misstatements, but it does not reach the depth of reasonable assurance applied to financial statements. Reasonable assurance may be phased in under future CSRD revisions.

The challenge for finance professionals is that many organizations report against multiple frameworks simultaneously. A company disclosing under both GRI and TCFD must reconcile different definitions of materiality and different metric requirements. Auditors then need to verify disclosures against each framework's specific criteria.

Pro Tip: Map your ESG metrics to each applicable framework before the audit begins. A simple matrix showing which metric satisfies which framework requirement saves significant time during evidence review.

| Framework | Materiality approach | Primary focus | Assurance relevance |

|---|---|---|---|

| GRI | Impact materiality | Stakeholder impacts | Widely used for ESG assurance scope |

| SASB | Financial materiality | Industry-specific metrics | Aligns with investor-focused audits |

| TCFD | Financial materiality | Climate risk disclosures | Increasingly required by regulators |

| CSRD | Double materiality | Financial and impact perspectives | Sets limited assurance as default |

What evidence and documentation are critical for successful ESG audits?

Auditors require a traceable evidence chain that links every reported ESG metric back to authentic source documents. This is the single most common area where organizations fall short. Treating ESG data as marketing content rather than financial-grade evidence creates audit failures that are entirely avoidable.

A strong evidence chain includes:

- Utility invoices and meter readings for Scope 1 and Scope 2 greenhouse gas emissions calculations

- HR records and payroll data for social metrics such as workforce diversity, pay equity, and turnover rates

- Board and committee minutes for governance disclosures including oversight structures and policy approvals

- Supplier contracts and audit certificates for supply chain and procurement-related disclosures

- Timestamped system logs showing when data was entered, by whom, and whether it was subsequently modified

Documented controls matter as much as the underlying data. An auditor who can see that a specific person reviewed and approved a data entry, with a date and sign-off, gains confidence in the figure. An undocumented spreadsheet with no version history raises immediate questions.

Stakeholder interviews complement documentary evidence by showing how governance actually operates. An interview with the sustainability director can confirm that the carbon accounting methodology described in the report is the one actually used. That corroboration strengthens the auditor's confidence beyond what documents alone can provide.

Finance professionals with ESG data management skills are well positioned to build and maintain this evidence chain. The discipline of financial reporting, where every number ties back to a source, transfers directly to ESG audit readiness.

What are best practices and common challenges in executing ESG audits?

ESG reporting now spans multiple business functions beyond the sustainability team, requiring clear ownership and cross-departmental coordination. Finance professionals who treat ESG audit preparation as a shared responsibility rather than a compliance task assigned to one team consistently achieve better outcomes.

The most common challenges finance teams face include:

- Inconsistent data collection across business units using different methodologies or definitions for the same metric

- Lack of documented controls leaving auditors unable to verify that data was reviewed before reporting

- Weak evidence management where source documents are stored informally and cannot be retrieved quickly during fieldwork

- Framework misalignment when reported metrics do not precisely match the definitions required by the applicable standard

- Late engagement with auditors, which compresses the timeline and limits the opportunity to resolve issues before the report is issued

Integrating ESG audit readiness with the existing financial audit cycle is one of the most effective structural improvements a finance team can make. Financial audits already require documented controls, traceable evidence, and management sign-off. Extending that discipline to ESG data reduces duplication of effort and builds on infrastructure that already exists.

Cross-functional training is equally important. Operations staff who understand why their utility data feeds into a carbon disclosure are more likely to maintain accurate records. Legal teams who understand CSRD scope are better prepared for governance-related interview questions. Finance professionals with ESG research skills can lead that internal education effort effectively.

Pro Tip: Assign a named data owner for each ESG metric at the start of the reporting cycle. When auditors ask who is responsible for a figure, a clear answer signals organizational maturity and reduces audit friction.

Key takeaways

A successful ESG audit depends on traceable evidence, clear data ownership, and early alignment with the applicable reporting framework before fieldwork begins.

| Point | Details |

|---|---|

| Five-phase structure | ESG audits follow scope, systems, evidence, testing, and reporting phases in sequence. |

| Framework drives scope | GRI, SASB, TCFD, and CSRD each define materiality differently, directly shaping what auditors test. |

| Evidence chain is critical | Every reported metric must trace back to source documents with documented controls and approvals. |

| Limited assurance is the current standard | CSRD defaults to limited assurance; reasonable assurance may be introduced in future revisions. |

| Cross-functional ownership improves outcomes | Assigning named data owners across departments reduces audit findings and speeds up fieldwork. |

Why ESG audits reward preparation more than any other compliance process

Finance professionals often ask me which part of the ESG audit process catches organizations off guard most consistently. The answer is always the evidence chain. Teams spend months preparing their ESG report, refining the narrative, and aligning metrics to frameworks. Then auditors arrive and ask for the utility invoice behind a specific emissions figure, and no one can find it.

The ESG due diligence process explained in most guides focuses on what to report. The harder question is whether you can prove it. I have seen well-resourced organizations with sophisticated sustainability programs fail limited assurance reviews because their data lived in informal spreadsheets with no version control and no documented methodology. The report looked credible. The evidence did not.

The fix is not complicated, but it requires starting early. Treat every ESG metric as if a financial auditor will ask for its source document on day one of fieldwork. Build that habit into your data collection process from the beginning of the reporting cycle, not three weeks before the audit starts.

The regulatory direction under CSRD is clear: assurance requirements will tighten, and the move toward reasonable assurance will raise the bar further. Organizations that build financial-grade evidence practices now will be far better positioned when that shift arrives. The ESG integration practices that work in financial reporting transfer directly to ESG audit readiness. Finance professionals are already trained for this. The task is applying that discipline to a new data set.

— Charles

Verdantinstitute: building ESG audit competency for finance professionals

Finance professionals who want to lead ESG audit readiness within their organizations need more than a checklist. They need a working understanding of frameworks, assurance standards, and evidence requirements.

Verdantinstitute offers structured learning tracks covering ESG analysis, sustainable finance, and compliance practice, with courses built specifically for finance practitioners. The platform's library of 16 courses and over 160 lessons includes deep dives into ESG reporting frameworks and assurance processes. CPD tracking and certifications make it practical for professionals managing ongoing development requirements. Plans start at $18 per month for students and $58 per month for professionals. Explore the full curriculum or review plan options and pricing to find the right fit for your role.

FAQ

What is the ESG audit process?

The ESG audit process is a structured, phased evaluation of a company's environmental, social, and governance disclosures to verify their accuracy and compliance with reporting standards such as GRI, SASB, TCFD, or CSRD. It typically covers five phases: scoping, data systems assessment, evidence gathering, substantive testing, and assurance reporting.

What is the difference between limited and reasonable assurance in ESG audits?

Limited assurance checks for material misstatements and provides a moderate level of confidence, while reasonable assurance requires deeper testing and is the standard applied to financial statements. CSRD currently defaults to limited assurance for ESG disclosures.

What documents do auditors request during an ESG audit?

Auditors typically request utility invoices for emissions data, HR records for social metrics, board minutes for governance disclosures, and supplier certificates for supply chain claims. Every reported metric must trace back to a source document with documented controls.

How does CSRD change the ESG audit scope?

CSRD applies double materiality, requiring organizations to assess both how ESG factors affect their financial performance and how their activities affect the environment and society. This dual lens significantly expands the scope of disclosures subject to assurance compared to single-materiality frameworks.

How can finance teams prepare for an ESG audit?

Finance teams should assign named data owners for each ESG metric, integrate ESG evidence collection with existing financial audit controls, and engage auditors at least three months before fieldwork begins. Inconsistent data collection and weak evidence management are the most common causes of audit findings.