ESG disclosure analysis techniques are structured methods combining natural language processing, machine learning, and regulatory scoring frameworks to evaluate the accuracy, completeness, and credibility of sustainability reporting. Finance professionals use these techniques to detect greenwashing, assess compliance with ESRS and IFRS S2, and extract investment signals from corporate sustainability disclosures. This article covers the core approaches in use in 2026, including NLP sentiment scoring, XGBoost with SHAP explainability, and ESRS IRO materiality assessment, giving you a practical framework to apply immediately.

What are the main ESG disclosure analysis techniques used in 2026?

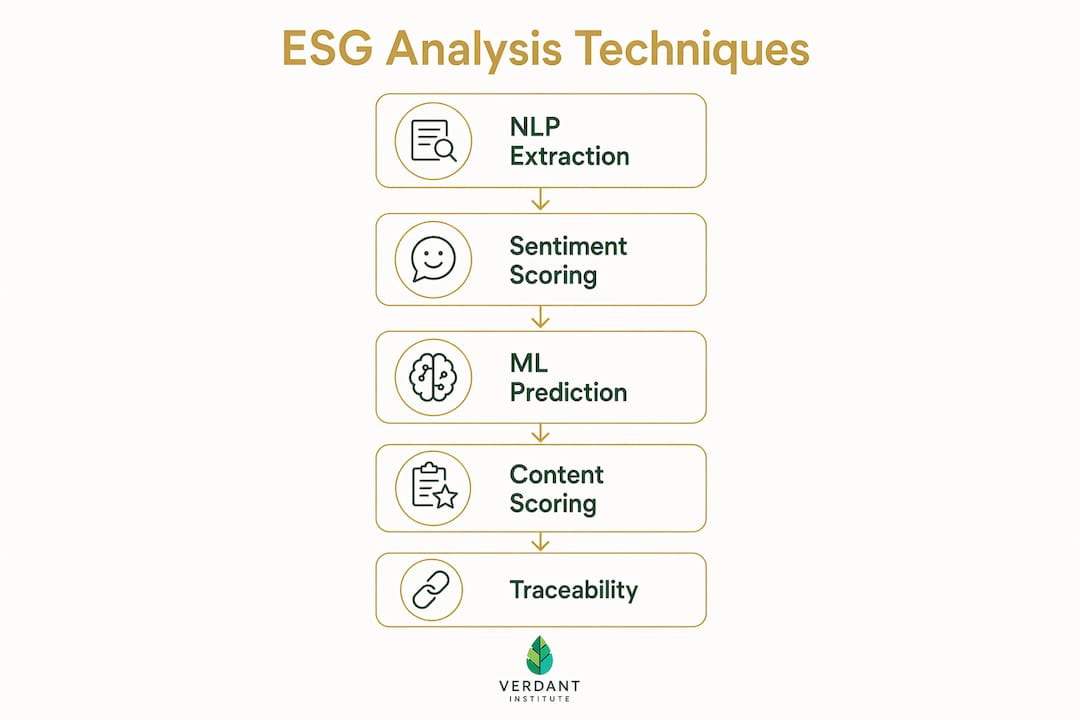

ESG disclosure analysis, known in practice as sustainability disclosure assessment, spans four distinct technique categories: NLP-based language analysis, machine learning prediction models, content-analysis scoring frameworks, and traceability systems for assurance preparation. Each addresses a different dimension of disclosure quality, and the strongest analytical workflows combine all four.

NLP-based approaches extract meaning from the text of sustainability reports. Sentiment analysis measures whether language is positive, neutral, or negative relative to environmental claims. Alignment scoring maps report language against the UN Sustainable Development Goals or sector-specific taxonomies to quantify how well stated commitments match recognized sustainability targets. The Greenwashing Tendency Score (GTS) combines NLP sentiment analysis, SDG alignment, and third-party ESG ratings into a single quantitative greenwashing risk measure, with scores ranging from 0.7 to 3. A score approaching 3 signals a significant gap between what a company says and what independent raters confirm.

Machine learning prediction models take this further by incorporating financial and governance features alongside text signals. An XGBoost model with SHAP achieves over 86% accuracy in predicting ESG greenwashing, with corporate financial characteristics proving more predictive than governance variables alone. This matters for analysts because it means balance sheet data and revenue structure carry real signal for disclosure credibility.

Content-analysis scoring frameworks apply topic taxonomies and rubrics to assess whether disclosures cover required topics at sufficient depth. Analysts score each disclosure element against defined criteria, producing a structured quality profile that is directly comparable across companies and reporting periods.

Traceability systems document the transformation logic behind every reported metric, from raw data source to final disclosed figure. This documentation is not just good practice. It is the foundation of assurance readiness, as external auditors require evidence that reported numbers are reproducible and defensible.

Pro Tip: Separate your communication indicators (sentiment, alignment scores) from actual performance indicators (third-party ESG ratings) before drawing conclusions. Mixing them without distinction is the most common source of false positives in greenwashing detection.

How to implement NLP and machine learning models for ESG analysis

Implementing a reproducible NLP and ML workflow for ESG disclosures requires five sequential steps. Each step builds on the last, and skipping any one of them degrades the reliability of your outputs.

-

Extract and clean report text. Pull sustainability report PDFs using tools like PyMuPDF or pdfplumber, then strip headers, footers, tables, and boilerplate legal language. Raw text from annual reports contains substantial noise, and unclean input directly reduces model accuracy.

-

Generate embeddings using pre-trained language models. Models like MPNet or BERT convert cleaned text into numerical vectors that capture semantic meaning. The ESGLens open-source pipeline uses a BERT regression model trained specifically to predict environmental scores from sustainability report text, providing a working reference architecture you can adapt.

-

Build supervised learning targets from third-party ESG scores. Discretizing continuous ESG rating scores into ranked bins aligns your model outputs with real scoring systems, making results directly usable for portfolio risk analysis and investment screening.

-

Train your classification or regression model. XGBoost performs well on tabular ESG features because it handles missing data and nonlinear relationships without extensive preprocessing. Train on a labeled dataset of disclosures with known greenwashing outcomes or third-party scores, then validate on a held-out test set.

-

Apply SHAP for feature-level explainability. SHAP local attribution identifies which specific features, whether leverage ratios, carbon intensity figures, or board composition metrics, drive each individual prediction. This transforms a black-box output into a defensible, auditable finding that you can present to investors or regulators.

Pro Tip: When training on ESG report text, always version-control your training data alongside your model weights. ESG rating methodologies change annually, and a model trained on 2023 scores may produce systematically biased predictions when applied to 2026 disclosures.

How to analyze ESG disclosures for regulatory compliance and assurance readiness

Regulatory compliance analysis requires a different mindset than predictive modeling. Here you are not predicting a score. You are verifying that a disclosure meets specific structural and methodological requirements set by ESRS under CSRD or IFRS S2 under ISSB.

ESRS IRO materiality assessment is the starting point for CSRD compliance analysis. The ESRS IRO framework requires companies to disclose their methodology for identifying material impacts, risks, and opportunities, including stakeholder consultation processes and the thresholds used to determine materiality. Qualitative thresholds are acceptable under ESRS, but only when the rationale is fully documented. Missing or stale rationale in a qualitative threshold is more damaging to disclosure quality than a minor numeric discrepancy, because it signals that the materiality process itself was not rigorous.

When you analyze a disclosure for ESRS compliance, check for these elements:

- Explicit description of the IRO identification methodology

- Evidence of stakeholder consultation, including which groups were consulted and how their input was weighted

- Clear threshold logic, whether quantitative or qualitative, with documented justification

- Disclosure of any changes to methodology between reporting periods

IFRS S2 climate scenario analysis introduces a specific disclosure obligation that many analysts misread. IFRS S2 Paragraph 22 mandates disclosure of management's interpretation of climate scenario resilience, not the scenario tables or technical methodologies themselves. Auditors assess whether management has drawn a credible, evidence-based conclusion about the company's resilience. A disclosure that presents scenario outputs without interpretation fails this requirement regardless of how sophisticated the underlying modeling is.

| Disclosure element | What analysts should verify |

|---|---|

| IRO methodology | Stakeholder consultation documented; threshold logic explained |

| Materiality thresholds | Rationale current and specific to reporting period |

| Climate scenario interpretation | Management conclusion on resilience explicitly stated |

| Transformation logic | Raw-to-reported metric trail documented with change logs |

| Assurance evidence pack | Traceability matrices present; sampling rationale for volatile metrics included |

Traceability documentation is the practical mechanism that connects your analysis to audit readiness. Build a traceability matrix that maps every disclosed metric back to its source data, the transformation steps applied, and the person responsible for each step. For volatile metrics, increase your sampling frequency to strengthen assurance confidence.

What are common challenges and best practices in ESG disclosure analysis?

The three most persistent challenges in ESG disclosure analysis are report volume and noise, subjective scoring inconsistency, and the communication-performance gap that enables greenwashing to go undetected.

Noise reduction is a prerequisite for any text-based analysis. Sustainability reports routinely run to 200 or more pages, and the majority of that text is not analytically relevant. RAG-based greenwashing detection pipelines address this by dropping 60 to 70 percent of sentences before extraction, using relevance gating to retain only sentences containing environmental claims. This dramatically reduces processing cost and improves signal quality.

Subjective scoring inconsistency undermines comparability across analysts and time periods. The solution is a structured scoring rubric with defined criteria for each disclosure element, applied consistently by all team members. Pair rubric-based scoring with inter-rater reliability checks, where two analysts independently score the same disclosure and differences are reconciled, to build a defensible, auditable record.

The communication-performance gap is the core mechanism of greenwashing. A company can publish highly positive, SDG-aligned language while its actual environmental performance, as measured by third-party raters, tells a different story. Separating communication indicators from performance indicators before drawing conclusions is the single most important methodological discipline in this field.

Best practices that address all three challenges:

- Apply relevance gating before any text extraction to filter non-claim sentences

- Classify claim types (commitment, achievement, target, policy) before linking claims to evidence

- Use Retrieval-Augmented Generation pipelines to match claims against citable evidence corpora rather than treating reports as unstructured text

- Build change logs into your documentation system so that updates to methodology or regulatory requirements are tracked and dated

- Review your scoring rubrics against updated ESRS and IFRS guidance at least annually

For analysts building ESG investment decisions, the combination of relevance gating, claim classification, and evidence linkage produces a far more reliable signal than raw sentiment scores alone.

Key takeaways

Effective ESG disclosure analysis requires combining NLP scoring, explainable machine learning, and regulatory compliance verification into a single, documented workflow.

| Point | Details |

|---|---|

| Separate communication from performance | Analyze sentiment and alignment scores independently from third-party ESG ratings to detect greenwashing accurately. |

| Use SHAP for model transparency | Apply SHAP attribution to XGBoost predictions so every greenwashing flag is traceable to specific financial or governance features. |

| Verify IFRS S2 interpretation, not just tables | Auditors assess management's resilience conclusion under Paragraph 22, not the scenario methodology itself. |

| Document IRO methodology in full | ESRS compliance requires stakeholder consultation records and threshold rationale, not just the final materiality list. |

| Gate relevance before text extraction | Drop 60 to 70 percent of report sentences using relevance filters before running NLP models to reduce noise and cost. |

Why explainability is the non-negotiable standard in 2026

I have spent considerable time working through ESG disclosure workflows, and the pattern I keep returning to is this: the analysts who produce the most credible outputs are not necessarily the ones using the most sophisticated models. They are the ones who can explain every step of their process to a skeptical auditor or investment committee.

The shift toward explainable AI in ESG analysis is not a technical preference. It is a regulatory and commercial necessity. Investors and regulators alike are no longer willing to accept a greenwashing risk score without understanding which features drove it. SHAP attribution solves this problem technically, but the discipline of building explainability into your workflow from the start, rather than retrofitting it at the end, is what separates analysts who produce defensible findings from those who produce interesting ones.

The other thing I would push back on is the tendency to treat regulatory compliance analysis as a checklist exercise. The ESRS IRO assessment and IFRS S2 interpretation requirements are not boxes to tick. They are signals about the quality of a company's internal sustainability governance. A disclosure that meets every formal requirement but offers no genuine insight into how management thinks about climate risk tells you something important about the organization. Learning to read that signal is a skill that no rubric fully captures, and it is where domain expertise and analytical technique combine to produce real investment value.

For analysts building these skills systematically, the ESG analyst career guide from Verdantinstitute covers the workflow and competency requirements in detail.

— Charles

Build your ESG analysis skills with Verdant Institute

Verdant Institute offers structured training designed specifically for finance professionals who need to move beyond surface-level ESG familiarity and into applied analytical practice. The platform's Deep Dive and Advanced Practice tracks cover NLP-based disclosure analysis, explainable AI methods, CSRD/ESRS compliance frameworks, and assurance readiness, with CPD tracking built in. Professional plans start at $58 per month and include access to over 160 lessons across 16 courses. If you are building or refining an ESG disclosure analysis workflow, the Verdant pricing page outlines the plan options that fit your role and learning objectives.

FAQ

What is the Greenwashing Tendency Score?

The Greenwashing Tendency Score (GTS) is a quantitative measure that combines NLP sentiment analysis, SDG alignment scoring, and third-party ESG ratings to assess greenwashing risk, with values ranging from 0.7 to 3.

How does SHAP improve ESG machine learning models?

SHAP local attribution identifies which specific financial or governance features drive each individual greenwashing prediction, making XGBoost model outputs transparent and defensible for investors and regulators.

What does IFRS S2 Paragraph 22 require from companies?

IFRS S2 Paragraph 22 requires management to disclose its interpretation of climate scenario resilience, not just scenario tables or methodologies. This interpretation is the primary focus of assurance review.

Why is ESRS IRO methodology documentation so important?

Under ESRS, missing or outdated rationale in materiality threshold documentation reduces disclosure quality more than minor numeric errors, because it signals a flawed materiality process rather than a data issue.

What is relevance gating in ESG text analysis?

Relevance gating is a preprocessing step that filters out non-claim sentences before NLP extraction, typically removing 60 to 70 percent of report text to reduce noise and improve the accuracy of greenwashing detection models.