ESG real estate analysis explained properly is not about checking boxes on a sustainability form. It is a structured method for evaluating how environmental, social, and governance factors affect asset value, risk exposure, and long-term investment performance. Regulatory scrutiny is intensifying, institutional capital flows are shifting toward sustainability-linked assets, and lenders are integrating ESG into credit underwriting decisions. If you are still treating ESG as optional reporting overhead, you are misreading where the market is heading.

Table of Contents

- Key takeaways

- Core components of ESG real estate analysis

- Why data coverage and quality define your ESG credibility

- Physical climate risk and resilience in property analysis

- Financial challenges and the regulatory environment

- My take on what actually moves the needle in ESG real estate

- Build your ESG real estate expertise with Verdantinstitute

- FAQ

Key takeaways

| Point | Details |

|---|---|

| ESG is a valuation input | Environmental, social, and governance factors directly affect asset pricing, financing terms, and risk assessments. |

| Data quality determines scoring | Portfolios with high empirical data coverage consistently outperform global ESG benchmarks in energy and emissions categories. |

| Physical risk needs three layers | Effective climate resilience analysis requires assessing asset location, infrastructure access, and tenant business continuity separately. |

| Regulatory pressure is real | SEC climate disclosure rules and evolving lender requirements mean ESG compliance timelines are already in motion. |

| Active management beats compliance | Treating ESG as a continuous process rather than a periodic report generates measurable differences in investment performance. |

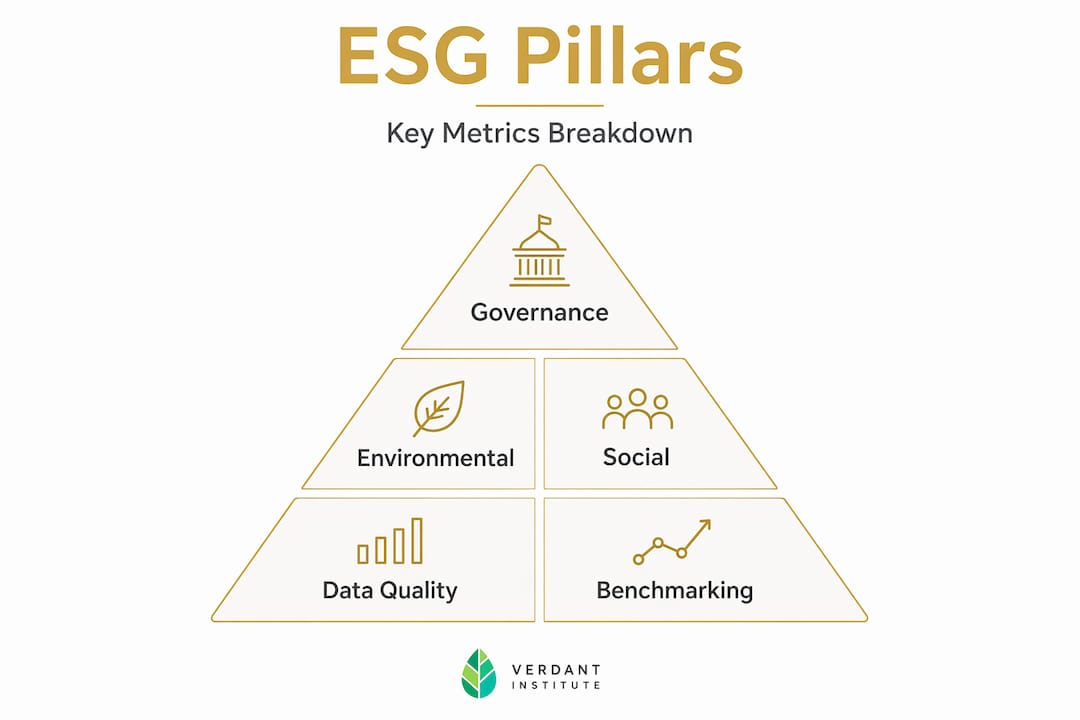

Core components of ESG real estate analysis

Understanding ESG in real estate starts with knowing exactly what gets measured. The three pillars each carry distinct metrics at the asset and portfolio level, and they do not carry equal weight across different scoring frameworks.

Environmental metrics are the most data-intensive pillar. Key performance indicators include energy consumption intensity, greenhouse gas emissions (scope 1 and 2 at minimum), water use, and waste diversion rates. These are not aspirational targets. They are quantitative inputs that feed directly into peer-group benchmarking and investor narratives tied to risk and value. A logistics asset consuming 40% more energy per square meter than its sector peer is not just an ESG problem. It is a cost risk and a re-leasing risk.

Social factors are harder to quantify but are gaining measurable traction. Tenant satisfaction surveys, health and safety incident rates, access to public transportation, and community investment programs all fall under this pillar. For commercial real estate specifically, tenant well-being metrics are starting to influence lease negotiations, particularly among large corporate occupiers with their own ESG commitments.

Governance covers how the organization operating the asset is managed. That includes sustainability policies, board oversight of ESG risks, data transparency, and engagement practices. According to GRESB scoring methodology, governance accounts for 66% of the governance component score, making policy quality and management processes genuinely decisive.

Here is a summary of the primary real estate ESG metrics by pillar:

| Pillar | Key Metrics | Data Source Examples |

|---|---|---|

| Environmental | Energy intensity, GHG emissions, water use, waste | Utility bills, smart meters, waste contractor data |

| Social | Tenant satisfaction, H&S incidents, community impact | Tenant surveys, incident logs, community reports |

| Governance | ESG policies, board oversight, reporting transparency | Internal policy documents, third-party audits |

Benchmarking across peer groups is where these metrics become investment-grade information. Without peer comparison, a single asset's energy score has limited analytical value. With it, you can identify underperformers, model upgrade scenarios, and communicate relative risk to capital partners.

Why data coverage and quality define your ESG credibility

The gap between a credible ESG score and a weak one almost always comes down to data. Specifically, it comes down to the proportion of your portfolio covered by measured data versus estimated data.

Portfolios with rigorous empirical data collection consistently produce stronger scores. High data coverage portfolios show energy data coverage of 97.8% compared to a global average of 78.6%, and GHG coverage of 97.8% against a 79.5% global average. That is not a marginal edge. It is a structural advantage in how investors and lenders read your ESG story.

The challenges are real and specific to real estate. Data is fragmented across asset types, geographies, and lease structures. Tenant-controlled spaces create gaps where landlords cannot access consumption data directly. Multi-tenanted buildings require sub-metering. Cross-border portfolios deal with inconsistent utility reporting standards.

What separates strong ESG teams from average ones is how they handle these gaps:

- Data governance protocols that specify who collects, validates, and approves consumption data before it enters the reporting system

- Audit trails that link reported figures back to original utility invoices or meter reads

- Estimation policies that document the methodology and boundaries for estimated data where measured data is unavailable

- Regular reconciliation between estimated and measured figures to reduce reliance on modeled numbers over time

The GRESB 2026 update adds further specificity. ESG teams must now align estimated and measured data by utility type, meaning a single aggregated energy figure will no longer be sufficient for credible scoring.

Pro Tip: Before your next reporting cycle, audit what percentage of your portfolio's energy data comes from actual meter reads versus estimates. A 10% improvement in measured data coverage can meaningfully shift your benchmark position.

The reputational and capital access risks of poor data are not hypothetical. Investors increasingly ask for data validation confidence before making allocation decisions, and lenders are building data quality requirements into ESG-linked loan covenants.

Physical climate risk and resilience in property analysis

Physical climate risk is where sustainable real estate analysis gets both the most consequential and most technically demanding. Climate extremes caused €822 billion in losses across Europe between 1980 and 2024. That figure alone should reframe how you approach acquisition due diligence.

The typical mistake is treating physical risk as a binary pass/fail filter tied to flood zone maps. Real resilience analysis requires three distinct layers, and collapsing them into a single hazard score misses critical exposure.

- Asset-level location risk: Is the building itself physically exposed to flooding, storm surge, extreme heat, or subsidence? This requires parcel-level modeling, not regional hazard averages. A building that sits 50 meters from a floodplain boundary needs a different analysis than one inside it.

- Infrastructure access risk: Can the asset continue operating if surrounding infrastructure is disrupted? Road access, power grid reliability, and water supply resilience all affect whether a building functions during and after a climate event, regardless of the building's own physical condition.

- Tenant business disruption risk: Even if the building survives intact, can your tenant operate? A manufacturing tenant dependent on a flood-prone supplier network faces income continuity risk that sits largely outside investor control but directly affects rental income.

"Business disruption risk often lies outside investor control but impacts income continuity heavily." — Responsible Investor

Integrating these three layers into acquisition models changes deal economics. A well-located industrial asset in a flood-risk corridor might still pass asset-level screening while failing on infrastructure and tenant continuity grounds. That nuance does not appear in macro-level climate models.

Practical integration means building physical risk scores into your underwriting templates, setting explicit acquisition constraints for high-risk hazard zones, and running climate scenario analysis for existing portfolio assets to identify where capex or insurance cost escalation is likely.

Financial challenges and the regulatory environment

Two forces are shaping ESG investment in property right now: investor cost anxiety and regulatory acceleration. Understanding both helps you build a more credible case for ESG integration.

On the cost side, the barriers are documented and specific. A 2025 RICS survey found that 49% of respondents cited financial uncertainty and cost concerns as top barriers to acquiring green buildings. The same proportion cited lack of ROI evidence, and 47% pointed to high initial costs. These are not irrational concerns. Green retrofits can carry significant upfront capital requirements, and the payback period depends heavily on energy pricing, lease structure, and occupancy profile.

The regulatory picture adds a timeline dimension that cost concerns cannot defer indefinitely. Here is where the major frameworks currently stand:

| Regulatory Driver | Scope | Status (2026) |

|---|---|---|

| SEC Climate Disclosure Rules | US public companies, large filers | Adopted 2024, stayed pending judicial review |

| EU SFDR / CSRD | EU fund managers and large corporates | Active, phase-in ongoing |

| GRESB Lender Assessment | Real estate lenders globally | Expanding adoption |

The SEC climate disclosure rules adopted in 2024 remain stayed pending judicial review, but large filers should already be building the data infrastructure required for phased emissions disclosure starting in 2025 and 2026. Waiting for legal certainty before building reporting capacity is a risk management failure.

Lenders are not waiting either. The GRESB Real Estate Lender Assessment evaluates borrower governance, portfolio performance, and ESG strategy quality. Loan pricing is beginning to reflect ESG performance differentials. That means a poorly documented ESG program is not just a reporting gap. It is potentially a higher cost of capital.

Pro Tip: Frame ESG data investment as balance sheet protection, not a reporting cost. When lenders price ESG risk into loan terms, the cost of poor data is measurable in basis points.

Translating ESG performance into investment narratives is where many real estate teams still struggle. The sustainable investing frameworks that institutional investors use to evaluate portfolios require specific, comparable, and auditable data. Anecdotal sustainability claims do not survive due diligence.

My take on what actually moves the needle in ESG real estate

I have seen a lot of ESG programs that look rigorous on paper and deliver almost nothing in practice. The pattern is almost always the same. Teams invest in a glossy sustainability report, collect the minimum data required for a benchmark submission, and then do very little with the results until the next reporting cycle.

What actually works is treating ESG as an active management discipline. The return on resilience framing gets it right: governance, environmental management, and stakeholder relationships generate measurable performance differences when they are embedded in day-to-day asset management decisions, not just reported annually.

In my experience, the teams that do this well share one habit. They use their ESG data between reporting periods. They track energy performance against budget monthly. They flag assets approaching risk thresholds before it becomes a capital issue. They brief acquisition committees on physical risk profiles before term sheets are signed.

The other pitfall I see repeatedly is treating physical climate risk as a standalone workstream. It belongs inside your core underwriting model. If your acquisition team and your sustainability team are producing separate documents that never formally merge, you are leaving material risk unquantified in your investment case.

The future of ESG factors in property valuation is not a separate "ESG premium." It is that non-ESG-compliant assets will face a discount as stricter energy performance regulations, tightening lender requirements, and corporate tenant ESG commitments reduce their market liquidity. That shift is already visible in certain European markets and is moving toward the US. Getting your ESG analysis infrastructure right now is not getting ahead of the curve. It is keeping pace with where institutional capital already is.

— Charles

Build your ESG real estate expertise with Verdantinstitute

If this article clarified the principles but left you wanting structured frameworks, Verdantinstitute offers exactly that. The ESG course library covers everything from foundational concepts to advanced topics like transition finance and net-zero strategies, all designed for finance professionals working in real estate and beyond.

Plans start at $18/month for students and $58/month for professionals, with CPD tracking and certifications included. If you are building the analytical skills to integrate ESG criteria for buildings into acquisition decisions, valuation models, and lender conversations, explore Verdantinstitute's pricing options and find the track that fits where you are in your career.

FAQ

What is ESG real estate analysis?

ESG real estate analysis is the process of evaluating environmental, social, and governance factors at the asset and portfolio level to assess risk, performance, and investment value. It uses quantitative metrics like energy intensity and GHG emissions alongside governance and social indicators.

How does data coverage affect ESG scores?

Higher empirical data coverage directly improves ESG benchmark scores. Portfolios with measured energy data coverage of 97.8% significantly outperform the global average of 78.6%, according to GRESB performance data.

What physical climate risks matter most in property analysis?

Flood risk, extreme heat, and storm exposure are the primary physical hazards, but credible analysis also requires assessing infrastructure access and tenant business disruption risk as separate resilience layers beyond the asset itself.

How are lenders using ESG in real estate decisions?

Lenders are integrating ESG into credit underwriting through frameworks like the GRESB Real Estate Lender Assessment, which evaluates governance, ESG strategy, and portfolio performance, with some institutions beginning to reflect ESG quality in loan pricing.

What are the biggest barriers to ESG real estate investment?

According to a 2025 RICS survey, financial uncertainty, lack of ROI evidence, and high upfront costs each rank as top barriers, cited by approximately 47 to 49% of respondents across European markets.