ESG stress testing investment portfolios is a structured process that quantifies potential portfolio vulnerabilities to environmental, social, and governance risks under extreme scenarios. Finance professionals now treat this discipline as a core component of risk management, not an optional add-on. European financial regulators finalized mandatory guidelines in january 2026 requiring ESG integration into supervisory stress tests using risk-based approaches. Those guidelines separate physical risks, transition risks, and other ESG factors across short- and long-term horizons. The result is a clear regulatory signal: portfolio resilience analysis must now account for climate shocks, policy shifts, and governance failures as distinct, measurable risk categories.

What is ESG stress testing for investment portfolios?

ESG stress testing, formally called climate and sustainability scenario analysis within supervisory frameworks, applies extreme but plausible ESG shocks to a portfolio to measure potential losses and concentration risks. The industry term used by the European Banking Authority and the European Insurance and Occupational Pensions Authority is "ESG stress testing," and it covers three primary risk categories: physical risks such as floods and wildfires, transition risks such as carbon pricing and stranded assets, and social and governance risks such as labor disputes and regulatory penalties. Each category behaves differently across asset classes and time horizons. A carbon tax shock hits energy equities within months, while a coastal flood risk may impair real estate holdings over decades. Treating these as a single ESG bucket produces misleading results.

The impact of ESG on portfolios is not uniform across sectors or geographies. A utility company in a coal-dependent region faces a fundamentally different transition risk profile than a renewable energy developer in Germany. Stress testing forces analysts to make those distinctions explicit rather than relying on aggregate ESG scores that mask location-specific and sector-specific vulnerabilities.

What prerequisites do you need before stress testing a portfolio?

A materiality assessment is the mandatory first step. This process identifies which ESG risks genuinely affect each asset class and geography in your portfolio, rather than applying blanket ESG metrics across all holdings. Without it, you waste modeling capacity on immaterial risks and miss the ones that actually move portfolio value. The 2026 EU joint guidelines from the European Supervisory Authorities make this step explicit and non-negotiable for regulated institutions.

Data quality is the second prerequisite, and it is where most programs fail. Asset-level and geolocated data granularity is critical to capture regional physical risks like floods and droughts that aggregated ESG scores routinely mask. A portfolio holding real estate investment trusts across coastal Florida and inland Ohio faces radically different flood exposure. Aggregated data treats both positions identically. Geolocated, asset-level data does not.

The table below compares the main methodological tool categories used in ESG stress testing programs.

| Tool category | Primary use case | Data requirement |

|---|---|---|

| Scenario modeling software | Running deterministic and Monte Carlo simulations | Asset-level financial and ESG data |

| Geospatial risk platforms | Mapping physical climate exposure by location | Geolocated asset data |

| ESG data providers | Supplying raw ESG scores, emissions, and controversy data | Issuer-level disclosures |

| Factor-based risk systems | Decomposing portfolio risk into ESG factor exposures | Holdings-level attribution data |

Pro Tip: Update your scenario library and underlying data at least once per year, and immediately after any material portfolio change or new regulatory guidance. Stale scenarios produce false confidence.

How do you design effective ESG stress test scenarios?

Scenario design is where most ESG stress testing programs introduce the most error. A professional framework includes at least three to four historical crisis replays, two to three hypothetical scenarios tailored to portfolio exposures, and single-factor sensitivity tests for each major risk driver, updated annually. Each scenario type serves a different analytical purpose.

The three scenario types work as follows:

- Historical replay scenarios apply the market dynamics of past crises, such as the 2008 financial crisis or the 2020 COVID shock, to your current portfolio. They reveal how existing holdings would have behaved under documented stress conditions.

- Hypothetical scenarios model plausible but unprecedented shocks, such as a sudden $200 per ton carbon price, a global biodiversity treaty that restricts land use, or a cascade of social unrest across emerging market supply chains.

- Single-factor sensitivity tests isolate one variable at a time, such as a 30% drop in water availability or a 50 basis point increase in the cost of capital for high-emission sectors, to identify which positions are most exposed to specific ESG drivers.

Beyond these three types, two additional approaches add depth to any ESG risk assessment program:

- Multi-factor scenarios combine physical and transition risks simultaneously. A scenario where a carbon tax coincides with a severe drought tests whether your portfolio's vulnerabilities compound or offset each other.

- Reverse stress testing works backward from a defined loss threshold to identify which scenarios would cause that loss. This reveals hidden vulnerabilities that forward-looking scenarios may not surface.

Scenario design bias often stems from anchoring on recent events. Analysts who lived through the 2022 energy crisis tend to overweight energy transition scenarios and underweight nature-related or social risks. A disciplined program forces scenario diversity by requiring at least one scenario that has no historical precedent.

Aligning time horizons matters as much as scenario selection. Short-term horizons of one to three years capture acute physical events and policy shocks. Long-term horizons of ten to thirty years capture structural transition risks and the compounding effects of governance failures. The 2026 EU guidelines explicitly require both horizons in regulated stress testing programs.

What methodologies apply to ESG stress test calculations?

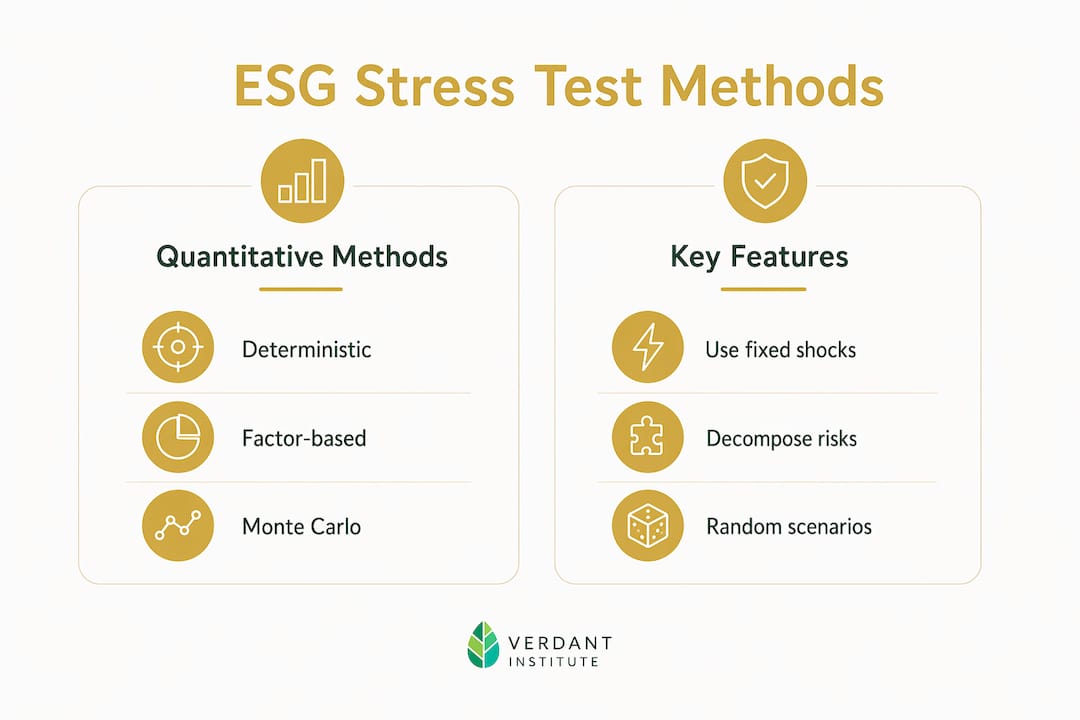

Three core quantitative methods power most ESG stress testing frameworks. Each has a distinct role, and the strongest programs use all three in combination.

Deterministic scenario analysis applies a fixed set of ESG shocks to the portfolio and calculates the resulting change in value. It is transparent and easy to communicate to investment committees, but it captures only the scenarios you explicitly define. It misses tail risks that fall between scenarios.

Factor-based stressing decomposes portfolio returns into ESG risk factor exposures and then stresses each factor independently. This method works well for identifying which holdings drive the most ESG-related risk, but it assumes linear relationships between factors and returns.

Monte Carlo simulations generate thousands of random scenarios based on specified ESG risk distributions. They produce a probability-weighted view of potential outcomes and provide better tail-risk insight than deterministic methods alone. Combining scenario analysis and Monte Carlo simulations gives analysts a fuller picture of extreme ESG risks than either method delivers on its own.

The choice between top-down and bottom-up modeling depends on your portfolio's complexity. Top-down modeling applies macro-level ESG shocks to the whole portfolio and works well for quick, high-level assessments. Bottom-up modeling starts at the individual security level and aggregates upward. It is more data-intensive but captures security-specific vulnerabilities that top-down approaches miss.

One critical technical consideration: linear ESG penalties increase portfolio concentration and reduce diversification, while nonlinear, ambiguity-driven adjustments preserve diversification. This means applying a flat ESG score penalty to all holdings below a threshold will push your portfolio toward a narrow set of high-scoring assets. Nonlinear adjustments, which shape uncertainty rather than penalize linearly, produce more stable and diversified portfolios under stress.

The comparison below summarizes the three main methodologies.

| Methodology | Strengths | Limitations | Data requirements |

|---|---|---|---|

| Deterministic scenario analysis | Transparent, easy to explain | Misses scenarios not explicitly modeled | Scenario-specific ESG shock inputs |

| Factor-based stressing | Identifies key risk drivers | Assumes linear factor relationships | Factor exposure data at holdings level |

| Monte Carlo simulation | Captures tail risks probabilistically | Computationally intensive | Full ESG risk distribution parameters |

Pro Tip: Validate your stress test outputs by comparing them against Value-at-Risk estimates. Stress testing complements VaR by targeting vulnerabilities that fall outside VaR's statistical assumptions, so large divergences between the two signal either a modeling error or a genuine blind spot in your VaR model.

How do you interpret results and apply them to portfolio management?

Stress test results indicate relative vulnerability, not absolute loss forecasts. This distinction matters because analysts frequently present stress test outputs as precise predictions, which overstates the certainty of any single scenario. The correct interpretation is: under this specific set of conditions, these holdings show the greatest sensitivity to ESG shocks.

Use results to identify three types of portfolio problems:

- Concentration risk: Holdings that cluster around the same ESG risk factor, such as multiple positions exposed to the same carbon pricing regime, amplify losses when that factor is stressed.

- Hidden correlations: Assets that appear uncorrelated under normal conditions may move together under ESG stress. A carbon tax shock can simultaneously impair energy equities, high-yield bonds from fossil fuel issuers, and infrastructure assets dependent on fossil fuel logistics.

- Nonlinear impact zones: Positions where a small increase in ESG stress produces a disproportionately large loss. These are the positions that linear models systematically underestimate.

Once you identify these vulnerabilities, the results feed directly into three portfolio management decisions. First, hedging: positions with extreme ESG sensitivity may warrant options, credit default swaps, or sector rotation to reduce exposure. Second, capital allocation: stress test results justify shifting capital away from high-vulnerability assets toward positions with lower ESG risk concentration. Third, rebalancing: ESG portfolio construction decisions should incorporate stress test findings as a standing input, not a one-time exercise.

The most common mistake analysts make is treating stress test results as a compliance deliverable rather than a management tool. A stress test that sits in a regulatory filing and never informs a trading or allocation decision has zero practical value. Stress testing is an ongoing discipline embedded in portfolio management, requiring updates after material portfolio changes or when new ESG risks emerge.

Key Takeaways

ESG stress testing requires a materiality-first approach, asset-level data, and a combination of deterministic, factor-based, and Monte Carlo methods to produce results that genuinely inform portfolio management decisions.

| Point | Details |

|---|---|

| Start with materiality | Identify which ESG risks actually affect your specific asset classes before building any scenario. |

| Use geolocated data | Aggregated ESG scores mask physical risk; asset-level and geolocated data reveal location-specific exposure. |

| Combine scenario types | Use historical replays, hypothetical scenarios, and sensitivity tests together for complete coverage. |

| Apply nonlinear adjustments | Linear ESG penalties reduce diversification; nonlinear methods preserve portfolio stability under stress. |

| Treat results as management input | Stress test findings should drive hedging, capital allocation, and rebalancing decisions, not just compliance reports. |

Why ESG stress testing is harder than most frameworks admit

I have spent years watching finance teams build technically correct ESG stress testing programs that produce almost no useful output. The problem is rarely the methodology. It is the assumption that a well-designed scenario library compensates for poor data. It does not. You can run the most sophisticated Monte Carlo simulation available, but if your underlying ESG data aggregates a coastal Florida REIT with an inland Ohio REIT into a single score, your output is fiction dressed as analysis.

The 2026 EU regulatory guidelines are a genuine step forward because they force institutions to separate physical, transition, and governance risks explicitly. But regulation sets a floor, not a ceiling. The analysts who get real value from stress testing are the ones who treat scenario design as a living process, not an annual checkbox. They update scenarios when a new carbon pricing mechanism passes, when a major biodiversity framework shifts land-use rules, or when a governance scandal reveals a systemic risk they had not modeled.

The other thing most articles on this topic miss: ESG stress testing and sustainable investing strategies are not the same discipline. Stress testing tells you where your portfolio breaks. Sustainable investing tells you where you want it to go. You need both, but confusing them produces a program that is neither rigorous risk management nor coherent investment strategy. Keep them separate, and let the stress test results inform the investment strategy rather than justify it after the fact.

— Charles

How Verdantinstitute supports your ESG stress testing practice

Finance professionals who want to build or sharpen their ESG stress testing capabilities need more than regulatory guidance. They need structured training that connects methodology to practice.

Verdantinstitute offers structured learning tracks covering ESG risk assessment, scenario design, and sustainable finance frameworks, all aligned with current regulatory standards including the 2026 EU joint guidelines. The platform's Deep Dive and Advanced Practice courses cover transition finance, net-zero strategies, and the quantitative methods that underpin credible stress testing programs. CPD tracking and certifications mean your professional development is documented and verifiable. Professionals can access the full course library for $58 per month. Review the full course and pricing options to find the track that fits your current role and compliance requirements.

FAQ

What is ESG stress testing for investment portfolios?

ESG stress testing is a structured process that applies extreme environmental, social, and governance shocks to a portfolio to measure potential losses and identify concentration risks. It covers physical risks, transition risks, and governance risks across short- and long-term time horizons.

What does the 2026 EU regulatory guidance require?

European financial regulators finalized guidelines in january 2026 mandating that institutions integrate ESG risks into supervisory stress tests using risk-based approaches, with explicit separation of physical risks, transition risks, and other ESG factors.

How is ESG stress testing different from Value-at-Risk?

VaR is model-based and relies on statistical assumptions about normal market behavior. Stress testing targets extreme scenarios that fall outside those assumptions, making the two methods complementary rather than interchangeable.

How often should ESG stress test scenarios be updated?

Scenarios should be updated at least annually and immediately after any material portfolio change or new regulatory development. Stale scenarios produce results that underestimate current risk exposure.

What is the biggest mistake in ESG stress test design?

The most common error is anchoring scenario design on recent events, which causes analysts to overweight familiar risks and miss novel or unprecedented ESG shocks. A disciplined program requires at least one scenario with no historical precedent.