Socially responsible investing is frequently reduced to a single idea: avoid bad companies. That framing is incomplete and, for finance professionals, potentially career-limiting. What is socially responsible investing at its full strategic depth? It is a framework that combines values-based screening, risk assessment, active ownership, and ethical investing principles to allocate capital with intention. The field now spans trillions of dollars globally and intersects with ESG analysis, impact mandates, and stewardship policies. Understanding where SRI begins and ends, and how it differs from adjacent strategies, is no longer optional for anyone working in or entering modern finance.

Table of Contents

- Defining socially responsible investing: core concepts and distinctions

- How socially responsible investing works: screening and implementation methods

- Understanding the nuances: comparing SRI, ESG, and impact investing approaches

- Challenges and opportunities in socially responsible investing today

- Applying socially responsible investing in professional practice

- A closer look: why typical SRI approaches may fall short and what can be done

- Enhance your socially responsible investing expertise with Verdant

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| SRI definition | Socially responsible investing channels capital into companies aligned with ethical, social, or environmental goals alongside financial returns. |

| Distinct strategies | SRI, ESG, and impact investing have overlapping but distinct approaches that affect outcomes and strategy design. |

| Implementation methods | Effective SRI uses negative screening, positive tilts, and stewardship to shape portfolios according to values. |

| Greenwashing risk | Transparency and credible disclosures are vital to avoid greenwashing and maintain investor confidence. |

| Practical application | Professionals must tailor SRI approaches to objectives and incentivize early positive change for real-world impact. |

Defining socially responsible investing: core concepts and distinctions

Socially responsible investing, commonly abbreviated as SRI, is more than a moral filter. Socially responsible investing allocates money into securities such as stocks, bonds, mutual funds, and ETFs that aim for positive social and environmental outcomes alongside financial returns. That dual mandate is what sets it apart from conventional investing. You are not simply chasing return. You are selecting instruments that align with a defined set of values while still targeting competitive performance.

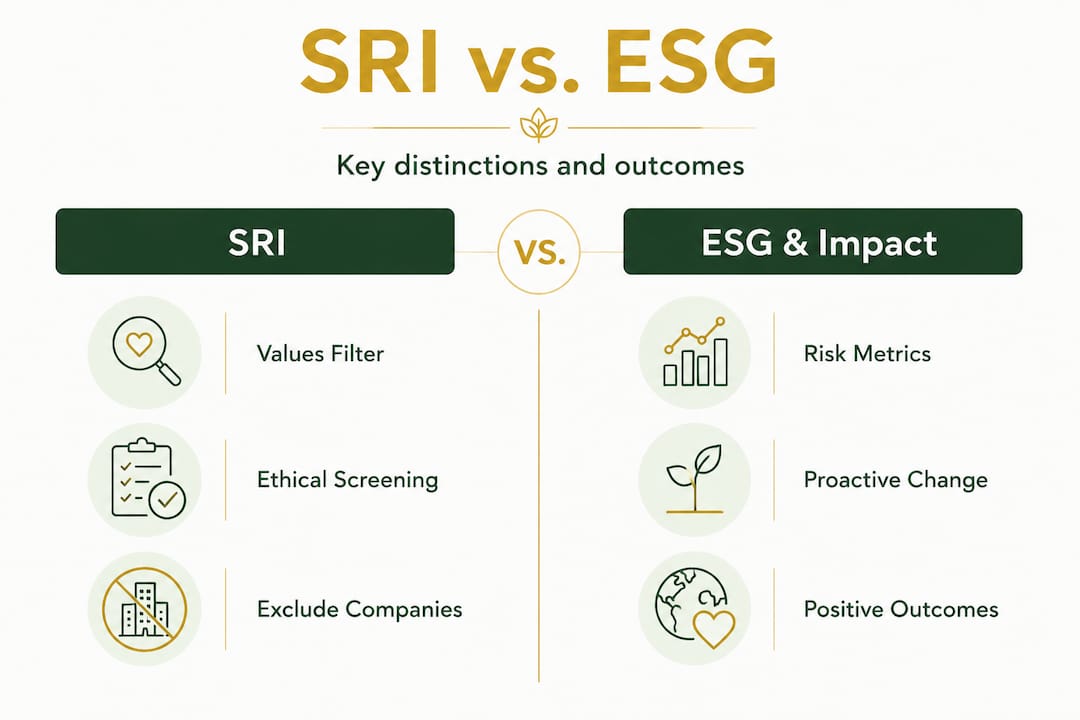

The distinction from ESG is one many professionals blur in practice. ESG investing evaluates a company's environmental, social, and governance practices as part of risk and opportunity assessment. It is primarily an analytical lens. SRI, by contrast, involves an active decision to include or exclude investments based on ethical criteria. Impact investing vs. SRI adds another layer: impact investing targets specific, measurable social benefits. It is outcome-oriented in ways SRI is not always required to be.

Here is a quick orientation to keep the three approaches distinct:

- SRI: Values-based screening, uses exclusions and inclusions to shape a portfolio in line with ethical criteria

- ESG: Risk and opportunity framework assessing company behavior on environmental, social, and governance factors

- Impact investing: Capital deployed to generate a specific, measurable social or environmental outcome alongside financial returns

Why does precision here matter? Because a client who wants their portfolio to "do good" may need an entirely different product depending on whether they mean "exclude weapons manufacturers," "favor high-ESG-scoring firms," or "fund affordable housing projects." Mismatching the mechanism with the objective is one of the most common sources of investor dissatisfaction. Reviewing a sustainable finance framework guide helps build the scaffolding to navigate these distinctions clearly.

How socially responsible investing works: screening and implementation methods

With SRI's definition clear, let's explore how these strategies are put into practice through concrete methods and frameworks.

The core implementation tool is screening. SRI screening uses criteria to either exclude certain investments or favor others based on specific ethical or ESG-related considerations. This might mean disqualifying companies that derive revenue above a threshold from tobacco, weapons, or fossil fuels. Or it might mean favoring companies that score highly on labor practices or board diversity metrics.

There are three primary screening modes:

- Negative screening: Excludes sectors or companies that conflict with defined values, such as gambling, alcohol, or carbon-intensive industries

- Positive/best-in-class screening: Selects the highest-performing companies within a sector on ESG or ethical metrics, rather than excluding the sector altogether

- Norms-based screening: Filters out companies that violate international standards such as the UN Global Compact or OECD guidelines

Beyond screening, active ownership is a powerful but underused tool. Engaging directly with company management on governance or environmental issues, filing shareholder resolutions, or exercising proxy votes can drive change without requiring divestment.

At the institutional level, the framework that shapes professional practice most is the UN Principles for Responsible Investment, which defines six voluntary principles covering ESG integration, active ownership, disclosure, and progress reporting. These principles guide how asset managers translate responsible investment goals into daily portfolio decisions.

| Screening type | Approach | Common use case |

|---|---|---|

| Negative screening | Excludes specific industries or companies | Avoiding fossil fuels, weapons, tobacco |

| Positive/best-in-class | Favors top ESG performers in each sector | Selecting leading companies within energy sector |

| Norms-based screening | Excludes firms violating international standards | Removing UN Global Compact violators |

| ESG integration | Incorporates ESG risk factors into analysis | Risk-adjusted return optimization |

| Active stewardship | Engages companies to improve practices | Shareholder resolutions on climate disclosure |

Pro Tip: When building or reviewing a socially responsible fund, look beyond the label and examine the methodology document. Funds using the same "SRI" label can differ enormously depending on whether they apply revenue thresholds, complete exclusions, or best-in-class tilts. The methodology is the product. You can explore more through Verdant's coverage of sustainable investing frameworks.

Understanding the nuances: comparing SRI, ESG, and impact investing approaches

Now that we have seen how SRI operates, let's examine how it compares and relates to ESG and impact investing within the sustainable finance landscape.

The three strategies are not interchangeable. They operate through different mechanisms and produce different outcomes. ESG investing looks at a company's environmental, social, and governance practices alongside traditional financial measures. It does not necessarily exclude any company. A high-ESG-score oil major may still appear in an ESG-integrated portfolio if its governance and environmental management are strong relative to peers.

SRI, on the other hand, applies a values filter that may not respond to ESG scores at all. A company could have excellent governance metrics but still be excluded under SRI criteria if it operates in an industry the investor has defined as out of bounds. These are fundamentally different decisions.

| Feature | SRI | ESG | Impact investing |

|---|---|---|---|

| Primary mechanism | Ethical screening | Risk and opportunity analysis | Targeted capital deployment |

| Typical vehicle | Mutual funds, ETFs | Equity portfolios, funds | Private equity, green bonds |

| Outcome focus | Values alignment | Financial performance | Measurable social benefit |

| Exclusion common? | Yes, frequently | Sometimes | Rarely |

| Measurement standard | Defined criteria | ESG ratings | Impact metrics (IRIS, GIIRS) |

For finance professionals advising clients, this table is not academic. It is practical. A client who says "I want ESG investing" may actually want SRI exclusions. A client who says "I want to make a difference" may need impact investing rather than either SRI or ESG integration. Accurately mapping client objectives to the correct ESG portfolio construction approach is a core advisory skill.

A few common misconceptions worth addressing directly:

- SRI does not guarantee lower financial returns compared to conventional portfolios

- ESG integration is not the same as ethical or values-based investing

- Impact investing is not a subset of SRI, even though they share socially conscious investing goals

- Green investing practices, such as targeting renewable energy funds, may fall under any of the three categories depending on implementation

Challenges and opportunities in socially responsible investing today

Having clarified SRI's relationship to other strategies, we now focus on the practical challenges and opportunities shaping its present and future.

Greenwashing sits at the top of every credible risk list in this space. Nearly one-third of investors cite greenwashing as a significant concern, and over three-quarters say the availability of sustainable investment options affects their choice of advisor or platform. That second statistic carries a clear professional implication: your ability to identify and communicate legitimate responsible investment options directly influences client retention.

Inconsistency in definitions and criteria across fund providers compounds the problem. Two funds labeled "socially responsible" may have completely different exclusion thresholds, different interpretations of what counts as "involvement" in a sector, and different update frequencies for eligibility rules.

"Professionals often assess SRI effectiveness not only at the portfolio level but at the benchmark and methodology levels: how exclusions are defined by revenues or thresholds, how involvement is measured, and how often the provider updates eligibility rules." Vanguard on SRI methodology

That layered assessment approach is what separates credible SRI analysis from surface-level label reading. When evaluating a fund, ask three questions. Does the screening methodology align with the stated ethical criteria? How are revenue thresholds defined and applied? How recently were exclusion rules reviewed?

Pro Tip: Subscribe to the regulatory output from ESMA, the SEC, and national financial regulators. The pace of greenwashing enforcement is accelerating, and staying ahead of disclosure requirements will differentiate you in both advisory and analytical roles. Verdant's coverage of ESG disclosure research is a strong starting point.

The opportunity side is equally real. Investor demand for responsible investment options is growing across retail and institutional segments. Finance professionals who can competently evaluate SRI strategies and communicate their mechanisms clearly are positioned well in an industry where that skill set remains scarcer than the job postings suggest.

Applying socially responsible investing in professional practice

To bring this full circle, here is how you actually implement SRI thinking in your day-to-day work, whether you are building portfolios, advising clients, or studying for a role in sustainable finance.

-

Clarify values and objectives first. Before selecting any screen or fund, map out your client's or your own ethical priorities. Matching terminology to objectives prevents misaligned incentives and misrepresented outcomes. "I want to avoid fossil fuels" and "I want to invest in solutions to climate change" are not the same instruction.

-

Select the screening approach that fits. Negative screening works for clear value-based exclusions. Positive/best-in-class screening is better when you want broad market exposure with an ethical tilt. Norms-based screening is appropriate when alignment with international standards is the priority.

-

Build active stewardship into the strategy. Voting proxies and engaging management is not a add-on. It is often where the most direct impact on company behavior occurs, particularly for large institutional holders.

-

Design incentives that reward early improvement. Research on investor incentives shows that exclusion-only approaches can inadvertently reward companies that delay improvements until they become ineligible for divestment. If measurable change is the goal, the incentive structure must reward early corporate reform, not just eventual compliance.

-

Pursue specialized education and certification. The field is moving quickly. Certifications in ESG analysis and sustainable finance signal credibility to employers and clients alike. A structured learning path accelerates what would otherwise take years of unguided exposure to get right. Explore how to achieve ESG certification as a foundational career step.

A closer look: why typical SRI approaches may fall short and what can be done

Here is the uncomfortable reality most SRI commentary skirts: exclusion-only strategies are often more about investor comfort than real-world change.

Research on SRI incentive structures shows that even well-intentioned SRI can fail to accelerate improvements when the portfolio structure rewards waiting rather than improving early. A company that knows it will be divested once its revenue from a disfavored activity crosses a threshold has limited incentive to reform before that point. The exclusion happens after the fact. The behavior that mattered occurred before the divestment decision.

This is not an argument against SRI. It is an argument for using it with clear eyes. Confusing the three implementation mechanisms, negative screening, positive tilts, and stewardship engagement, is the primary reason investors feel misled by products marketed under the ESG or SRI umbrella. The mechanism determines what you can reasonably expect the investment to change.

For professionals advising clients on socially conscious investing, the practical implication is this: if a client wants their capital to change corporate behavior, passive exclusion is unlikely to deliver that outcome on its own. Engagement strategies, impact-linked fund structures, or explicit measurable goals are often required. Understanding sustainable investing frameworks in depth is what allows you to advise with that level of precision rather than defaulting to whichever fund has the most legible label.

The most valuable thing you can do for a client asking about socially responsible investing is not to show them a list of screened funds. It is to understand what they actually want to change, and then select the mechanism most likely to change it.

Enhance your socially responsible investing expertise with Verdant

The gap between understanding SRI conceptually and applying it confidently in practice is where most professionals stall. Verdant Institute is built to close that gap.

At Verdant Institute, you will find structured learning tracks covering SRI, ESG integration, impact investing, and transition finance, supported by CPD tracking and industry-recognized certifications. Students access the full library for $18 per month. Professionals can unlock advanced practice content for $58 per month. Whether you are building your foundational knowledge or going deeper into methodology and portfolio construction, Verdant's sustainable investing courses give you the frameworks the industry actually uses. Review Verdant's pricing options and start building skills that hold up under scrutiny.

Frequently asked questions

What is the main difference between socially responsible investing (SRI) and ESG investing?

SRI uses specific ethical criteria to include or exclude investments, while ESG investing evaluates companies on environmental, social, and governance risks and opportunities alongside financial metrics. One is a values filter; the other is an analytical framework.

How can finance professionals avoid greenwashing when recommending socially responsible investments?

Carefully assess underlying holdings, screening criteria, and the transparency of any sustainability claims, and prioritize funds with verified impact disclosures and reporting. Methodology documents matter more than marketing labels.

What role does the UN Principles for Responsible Investment (UN PRI) play in socially responsible investing?

UN PRI provides a voluntary six-principle framework guiding investors on ESG integration, active ownership, and disclosure to promote responsible investment practice across asset classes.

Can socially responsible investing generate competitive financial returns?

Yes. SRI targets positive outcomes alongside financial returns, and a growing body of evidence shows screened portfolios can perform competitively, though results vary based on screening criteria and market conditions.