ESG compliance obligations are the mandated rules and standards organizations must meet to measure, manage, and report their environmental, social, and governance performance. In 2026, these obligations have shifted from voluntary best practices to legally enforceable requirements with real financial penalties. The EU's Corporate Sustainability Reporting Directive (CSRD) now covers nearly 50,000 companies, while California SB 253 targets U.S. firms with over $1 billion in revenue. Getting ESG compliance obligations explained clearly is no longer optional for finance professionals, corporate controllers, or sustainability officers. Structured governance, verified data, and third-party assurance are now the baseline.

What are the key ESG regulatory frameworks in 2026?

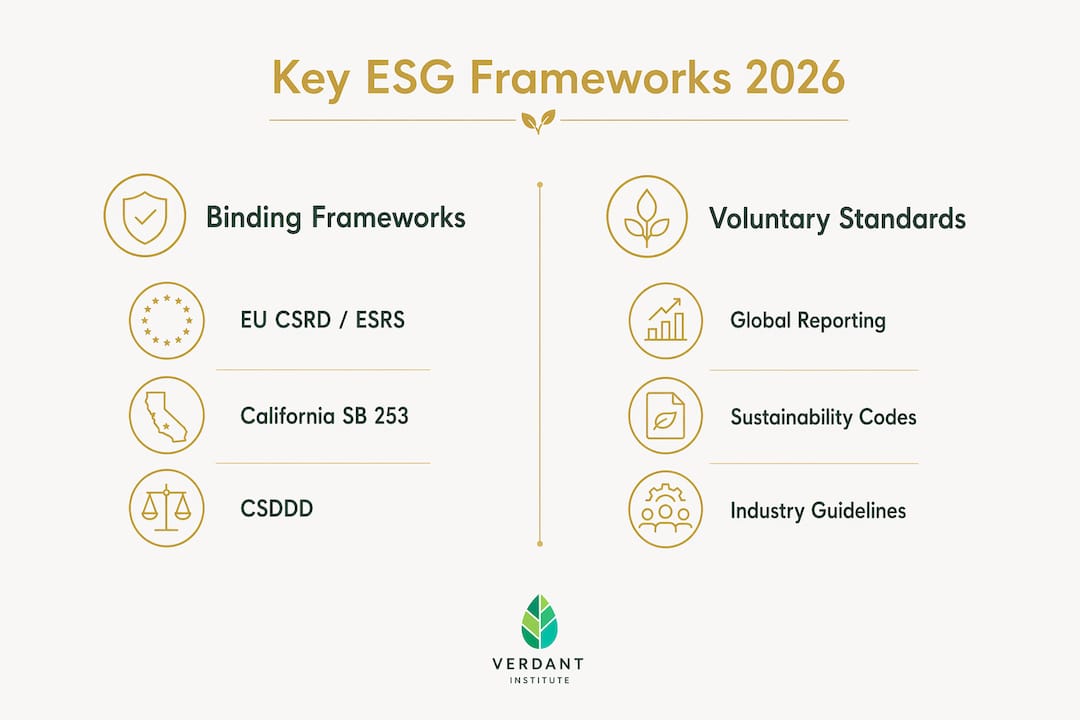

The global ESG regulatory picture in 2026 is defined by a small number of binding frameworks that carry real legal weight. Understanding each one is the foundation of any credible ESG regulatory compliance checklist.

The EU CSRD and ESRS

The ESRS standards were adopted in july 2023 and are mandatory for in-scope companies from 2024 onward, covering environmental, social, and governance topics under a single binding framework. The CSRD requires companies to report against these standards with phased assurance requirements. Initial filings require limited assurance, progressing toward reasonable assurance for the largest 10,000 companies and non-EU parent companies with significant EU operations. This progression matters because it means the audit bar rises every year, and companies that treat early filings as low-stakes are building a compliance gap they will have to close under pressure.

California SB 253 and u.s. state laws

California SB 253 mandates that companies with over $1 billion in annual revenue disclose Scope 1 and Scope 2 greenhouse gas emissions starting in 2026, with Scope 3 reporting required from 2027. Non-compliance carries penalties of up to $500,000 per year. Scope 3 emissions typically account for 70–90% of a company's total carbon footprint, which is why regulators are pushing hard to include them. New York's SB 9072 follows a similar model, signaling that U.S. state-level ESG compliance requirements will continue to expand regardless of federal direction.

CSDDD, EUDR, and global voluntary standards

The Corporate Sustainability Due Diligence Directive requires companies to prevent human rights and environmental harms across global value chains, with national transposition deadlines set for july 2026. The EU Deforestation Regulation (EUDR) adds commodity-specific obligations for companies trading in cattle, soy, palm oil, and other high-risk goods. Alongside these hard laws, frameworks like the International Sustainability Standards Board (ISSB) and the Global Reporting Initiative (GRI) function as operational baselines. Hard law regulations like CSRD carry immediate legal consequences, while voluntary standards like ISSB and GRI are increasingly expected by institutional investors even where not legally required.

| Framework | Scope | Key Requirement | Enforcement |

|---|---|---|---|

| EU CSRD / ESRS | ~50,000 companies | ESRS-based disclosures with assurance | EU member state regulators |

| California SB 253 | $1B+ revenue U.S. firms | Scope 1, 2, and 3 GHG disclosures | Up to $500,000/year penalty |

| CSDDD | Large EU and non-EU companies | Supply chain due diligence | National transposition by july 2026 |

| ISSB / GRI | Voluntary, global | Sustainability disclosures | Investor and market pressure |

How does double materiality shape ESG obligations?

Double materiality is the principle that determines what a company must report. It is not optional framing. Under the CSRD and ESRS, double materiality requires reporting on both the financial risks ESG factors pose to the company and the company's own impacts on the environment and society.

This two-directional test removes the ability to cherry-pick favorable topics. A company cannot report only on climate risks to its own revenue while ignoring the emissions it generates. A topic must be reported if it meets either the financial materiality threshold or the impact materiality threshold. Meeting only one is sufficient to trigger the obligation.

The practical implications of this are significant:

- Financial materiality covers ESG risks and opportunities that affect the company's cash flows, access to capital, or cost structure.

- Impact materiality covers the company's actual or potential effects on people, ecosystems, and communities, regardless of whether those effects feed back into financial performance.

- Documentation requirements mean companies must show their methodology for assessing both dimensions, not just their conclusions.

- Stakeholder input is part of the assessment process under CSRD, meaning companies cannot conduct materiality assessments in isolation.

The challenge most companies underestimate is the documentation burden. Regulators and auditors do not just want the final materiality matrix. They want to see the process, the data sources, the stakeholder consultations, and the rationale for topics that were excluded. For financial firms navigating sustainability risk, double materiality adds a layer of complexity that sits at the intersection of risk management and disclosure governance.

Pro Tip: Build your materiality assessment in a format that can be shared directly with auditors. If your documentation lives in slide decks and email threads, you will spend significant time reconstructing it under assurance review.

How do you manage ESG data and governance for compliance?

ESG data governance is where most compliance programs succeed or fail. The shift to auditable, data-driven ESG reporting is a defining trend in 2026. Companies without third-party verified data face greenwashing accusations and growing enforcement risk.

The core requirement is traceable data lineage. Every number in an ESG report must be traceable back to its source, through every calculation step, to the raw data. Auditors call this the "source to report" trail. If you cannot reconstruct how a figure was derived, it will fail under assurance review.

Here is a structured approach to building compliance-grade ESG data governance:

- Establish a single source of truth. All ESG data must flow from one controlled system, not from multiple spreadsheets maintained by different business units. Fragmented data is the most common cause of audit failures.

- Apply the four-eyes principle. Internal controls and sign-offs require that data entry and data review are performed by different individuals. This mirrors financial reporting controls and is explicitly expected under CSRD assurance processes.

- Standardize calculation methods. Inconsistent emissions factors or shifting methodologies between reporting periods trigger immediate audit issues. Document your chosen methodology and apply it consistently.

- Map data lineage formally. Tracing ESG data from source to report is not just good practice. Inability to trace numbers is a direct cause of assurance failures.

- Plan for ESEF digital tagging early. ESG reporting in ESEF format requires taxonomy tagging and technical coordination between IT, compliance, and reporting teams. Companies that leave this to the final weeks before filing face vendor delays and significant unplanned costs.

Pro Tip: Treat your ESG data controls audit as a dry run six months before your actual filing deadline. Identify gaps in lineage documentation and sign-off trails while you still have time to fix them.

For finance professionals looking to build deeper fluency in ESG disclosure analysis, understanding the governance layer behind the numbers is as important as knowing the reporting standards themselves.

How can businesses manage supplier and stakeholder ESG engagement?

Supply chain oversight is now a formal legal obligation, not a reputational preference. The CSDDD requires large companies to conduct risk-based due diligence across their entire value chain, identifying and addressing actual or potential adverse human rights and environmental impacts. National transposition deadlines in july 2026 mean enforcement timelines are real.

Companies that integrate supplier engagement into their ESG compliance frameworks consistently show better supply chain risk mitigation and lower reputational exposure. The key is treating supplier engagement as a structured process, not a one-time questionnaire.

Effective supplier and stakeholder engagement under ESG compliance requirements includes:

- Risk-based prioritization. Not all suppliers carry equal ESG risk. Tier suppliers by geography, commodity type, and sector to focus due diligence where exposure is highest.

- Documented grievance mechanisms. CSDDD requires companies to establish channels through which workers and affected communities can raise concerns. These must be operational, not just written into policy.

- Supplier codes of conduct. Written standards that suppliers must meet, covering labor rights, environmental practices, and anti-corruption, form the contractual foundation of due diligence.

- Ongoing monitoring, not one-time audits. Compliance is a continuous process. Annual supplier audits are a floor, not a ceiling. High-risk suppliers may require quarterly reviews or on-site assessments.

- Transparent public disclosure. CSRD and CSDDD both require companies to disclose their due diligence processes and findings publicly. Vague statements about "supplier standards" no longer satisfy regulators or investors.

Understanding ESG obligations at the supply chain level also requires knowing which commodities trigger specific rules. Under the EUDR, companies trading in soy, cattle, palm oil, wood, cocoa, coffee, or rubber must verify that products are not linked to deforestation. This adds a traceability requirement that goes beyond standard supplier questionnaires.

Key takeaways

ESG compliance in 2026 is a legally binding, auditable obligation that requires governance structures equal in rigor to financial reporting.

| Point | Details |

|---|---|

| Major frameworks are binding | CSRD, SB 253, and CSDDD carry legal penalties, not just reputational risk. |

| Double materiality removes cherry-picking | Companies must report on both financial risks and their own impacts on society and environment. |

| Data lineage is non-negotiable | Every ESG figure must trace back to its source to pass third-party assurance review. |

| Supplier engagement is a legal duty | CSDDD requires documented, risk-based due diligence across global value chains. |

| Digital tagging needs early planning | ESEF taxonomy requirements demand IT, compliance, and reporting coordination well before deadlines. |

The compliance gap most organizations are still ignoring

After working in sustainable finance education for years, the pattern I see most often is not ignorance of the regulations. Most professionals know CSRD exists. The real gap is the assumption that ESG reporting can be managed the same way it was in 2021, with a small sustainability team pulling together a narrative report once a year.

That model is finished. The gap between self-reported and verified ESG data now exposes companies to greenwashing enforcement and investor litigation. What surprises me is how many organizations still treat data governance as a technical afterthought rather than a board-level priority. Failing to apply governance rigor equal to financial reporting produces weak data confidence and audit failures. I have seen this play out repeatedly.

My strongest advice is this: start with your data architecture, not your disclosure narrative. The companies that will navigate the 2026 compliance wave with the least disruption are the ones that built traceable, controlled data systems two years ago. If you are starting now, prioritize the four-eyes principle, standardized calculation methods, and ESEF readiness before you write a single sentence of your sustainability report. ESG compliance is governance work. Treat it that way.

For professionals who want to build the skills to lead this work, understanding why ESG matters in finance is the starting point for making the case internally.

— Charles

Build your ESG compliance skills with Verdantinstitute

Verdantinstitute is built specifically for finance professionals and sustainability practitioners who need more than a general overview of ESG. The platform offers structured learning tracks covering ESG foundations, deep dives into specific regulatory frameworks, and advanced practice areas including transition finance and net-zero strategies.

With over 160 lessons across 16 courses, Verdantinstitute provides CPD tracking and certifications that demonstrate compliance-grade expertise to employers and clients. Plans start at $18 per month for students and $58 per month for professionals. If you are preparing for CSRD filings, building internal ESG governance, or advising clients on regulatory readiness, explore Verdantinstitute's full course library to find the right learning track for your role.

FAQ

What are ESG compliance obligations?

ESG compliance obligations are the legally mandated requirements for organizations to measure, disclose, and manage their environmental, social, and governance performance. In 2026, major frameworks including the EU CSRD, California SB 253, and CSDDD define these obligations with binding legal force.

Which companies must comply with the EU CSRD?

The CSRD covers nearly 50,000 companies, including large EU-based firms and non-EU parent companies with significant EU operations. Reporting is phased, with the largest companies filing first and smaller in-scope entities following in subsequent years.

What is double materiality in ESG reporting?

Double materiality requires companies to report on both the financial risks ESG factors pose to the business and the company's own impacts on the environment and society. A topic triggers a reporting obligation if it meets either threshold, not both.

What penalties apply for ESG non-compliance?

California SB 253 imposes penalties of up to $500,000 per year for non-compliant companies. EU member state regulators enforce CSRD violations under national law, with penalties varying by jurisdiction.

How does CSDDD affect supply chain management?

The CSDDD requires large companies to conduct risk-based due diligence across their global value chains to identify and address human rights and environmental harms. National transposition deadlines fall in july 2026, making supply chain documentation and grievance mechanisms a near-term legal priority.