Impact investing is defined as the deliberate allocation of capital to generate measurable social or environmental impact alongside a financial return, making it fundamentally different from philanthropy, which prioritizes social benefit without any expectation of repayment. Understanding the difference between impact investing and philanthropy is no longer just academic. Investors and donors who grasp this distinction can deploy capital more deliberately, avoid common structural mistakes, and build portfolios that serve both legacy and financial goals. The Global Impact Investing Network (GIIN) identifies intentionality and measurement as the two non-negotiable pillars of any credible impact investing strategy.

Impact investing vs philanthropy explained: the core distinction

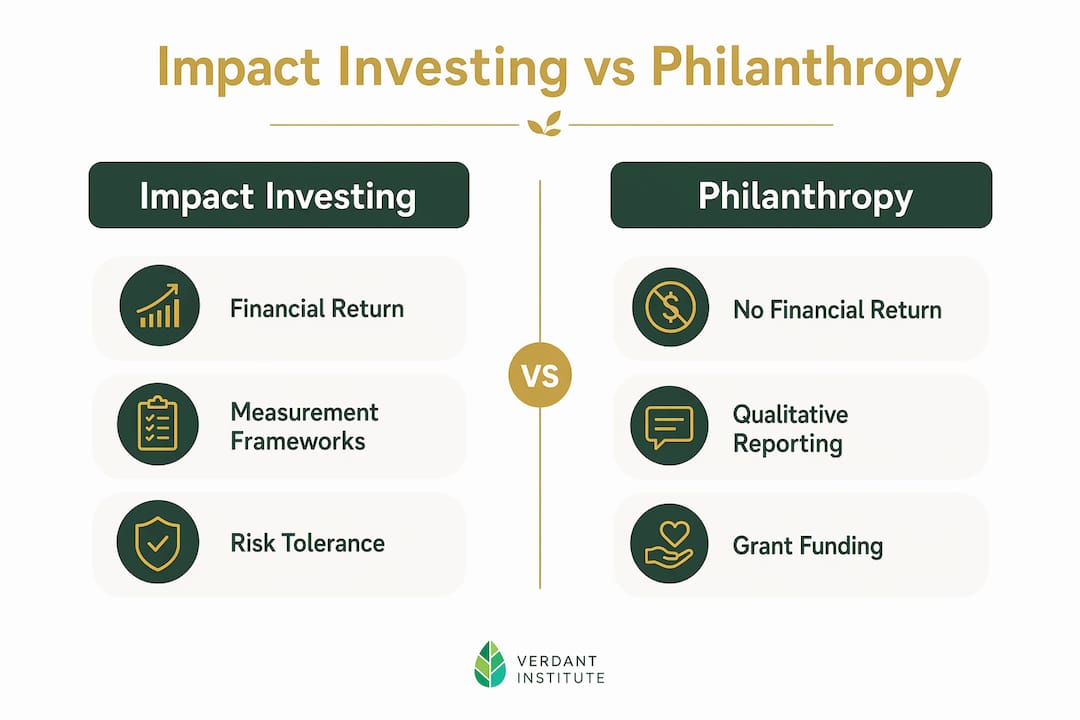

The single most important difference between impact investing and philanthropy is the expectation of financial return. Impact investing requires dual intent: measurable social or environmental outcomes plus a financial return, whether at market rate or below. Philanthropy, by contrast, delivers capital as grants or donations with no expectation of repayment.

That distinction shapes everything downstream. Risk tolerance, measurement frameworks, legal structures, and time horizons all follow from whether capital is expected to come back. A donor writing a check to a food bank is practicing philanthropy. A fund manager allocating to affordable housing bonds with a target return is practicing impact investing. Both serve social goals. Only one expects capital recovery.

90% of impact investors reported meeting or exceeding their financial return expectations in a 2022 GIIN survey. That figure directly challenges the assumption that doing good requires sacrificing returns.

How do financial expectations differ between the two approaches?

Impact investing targets returns across a wide spectrum. Market-rate impact investors expect returns competitive with traditional assets. Impact-first investors accept below-market returns to reach projects that commercial capital will not touch. Philanthropy sits at the far end of the spectrum, with zero return expectation.

The financial performance data favors impact investing more than most donors expect. Sustainable funds generated a median 12.5% return versus 9.2% for traditional funds in the first half of 2025. Impact-focused real estate funds saw net operating income increases of up to 13% annually, driven by tenant stability. These numbers matter because they reframe the conversation: impact investing is not a charitable concession. It is a competitive asset class.

Impact-first investing does carry a real cost. Miller Center research shows an impact-first premium of approximately $0.13 per dollar invested. Catalytic capital, often provided by philanthropic sources, frequently represents more than 50% of the funding stack that makes these deals viable. That means philanthropy and impact-first investing are not competing strategies. They are often co-dependent.

Pro Tip: If you are an investor evaluating impact-first deals, model the catalytic capital layer explicitly. Assuming commercial terms on the full stack will kill viable deals before they reach your desk.

What frameworks measure impact in investing versus philanthropy?

Impact investing relies on structured measurement frameworks. IRIS+ and the Impact Management Project are the two most widely adopted standards. IRIS+ provides a catalog of standardized metrics across sectors. The Impact Management Project offers a five-dimension framework covering what, who, how much, contribution, and risk. Together, they give investors a shared language for comparing outcomes across funds.

Philanthropy typically relies on qualitative outcome reporting. Grant recipients submit narrative reports, case studies, and anecdotal evidence of change. This is not inherently inferior. For early-stage social interventions where quantification is premature, qualitative data is often more honest than forcing numbers onto complex human outcomes.

The core challenge is comparability. Comparability across funds is limited, exposing investors to greenwashing risk without deep due diligence. Self-reported impact data, whether from a fund manager or a nonprofit, requires scrutiny. The Impact Management Platform addresses this by emphasizing iterative measurement processes where impact data continuously informs decisions, not just annual reporting cycles.

Practical metrics used in impact investing include:

- Jobs created per $1 million invested, common in workforce development funds

- Tons of CO2 avoided, standard in climate-focused portfolios

- Number of patients served, used in global health impact bonds

- Affordable units delivered, the primary metric in housing impact funds

- Students reached, tracked in education-focused social enterprises

Philanthropy uses similar output metrics but rarely ties them to capital efficiency or return calculations. That gap is where impact investing adds a layer of financial discipline that pure grant-making cannot replicate.

What is venture philanthropy and how does it relate to impact investing?

Venture philanthropy is a hybrid model that blends the capital-building focus of impact investing with the social mission of traditional philanthropy. Venture philanthropy focuses on social causal investments with typical durations of 3–7 years, emphasizing organizational capacity strengthening and performance measurement alongside grant funding.

The key difference from traditional philanthropy is engagement depth. A venture philanthropist does not just write a check. They provide technical assistance, governance support, and sometimes equity-like instruments to help a social enterprise become financially self-sustaining. The goal is to graduate the organization from grant dependency toward earned revenue or investment readiness.

Compared to impact investing, venture philanthropy accepts longer time horizons and lower financial return expectations. It sits between pure philanthropy and impact-first investing on the capital continuum. The table below maps the three approaches across key dimensions.

| Dimension | Philanthropy | Venture philanthropy | Impact investing |

|---|---|---|---|

| Financial return | None expected | Partial or none | Below-market to market-rate |

| Time horizon | Ongoing or project-based | 3–7 years | 5–10+ years |

| Capital instrument | Grants, donations | Grants plus capacity support | Debt, equity, bonds |

| Measurement focus | Qualitative outcomes | Performance metrics plus capacity | Quantitative, IRIS+ aligned |

| Primary goal | Social benefit | Organizational sustainability | Dual financial and social return |

Pro Tip: Venture philanthropy works best when the social enterprise has a clear path to earned revenue. Without that path, you are funding operations indefinitely, which is traditional philanthropy with extra steps.

How can investors and donors integrate both approaches for better outcomes?

The impact continuum framework treats philanthropic capital, impact-first capital, and market-rate capital as complementary tools rather than competing choices. The most effective impact portfolios use all three, deployed at different stages of a project's lifecycle.

Capital stacking is the practical application of this idea. A housing development might receive a philanthropic grant to cover predevelopment costs, an impact-first loan at below-market rates to close the financing gap, and a market-rate equity investment once the project is de-risked. Each layer serves a purpose. Removing any one layer often kills the deal entirely.

A practical integration framework follows four steps:

- Define your goals clearly. Separate your financial return targets from your impact objectives. Write both down. Conflicts between them are easier to manage when they are explicit.

- Map your capital to the continuum. Identify which portion of your portfolio can accept below-market returns and which requires market-rate performance. This determines where philanthropic and impact-first instruments fit.

- Embed impact across all capital, not just the impact bucket. Separating impact and investment buckets is a structural mistake. ESG integration in your market-rate holdings reduces risk and improves alignment with your stated values.

- Build feedback loops into your measurement process. Intentionality in impact investing requires iterative feedback, not just annual reporting. Adjust allocations based on what the data shows, not just what the thesis predicted.

The most common mistake investors and donors make is treating philanthropy and impact investing as separate silos managed by different teams with different goals. That structure guarantees misalignment. The impact capital continuum works only when the full portfolio is viewed as a single system.

Key takeaways

Impact investing and philanthropy are not opposites. They are complementary tools on a single capital continuum, and the most effective donors and investors use both deliberately.

| Point | Details |

|---|---|

| Dual intent defines impact investing | Impact investing requires both measurable social outcomes and financial return, unlike philanthropy. |

| Financial performance is competitive | Sustainable funds outperformed traditional assets in H1 2025, with median returns of 12.5% versus 9.2%. |

| Catalytic capital bridges the gap | Impact-first deals often require philanthropic capital covering 50%+ of the funding stack to become viable. |

| Measurement frameworks matter | IRIS+ and the Impact Management Project provide standardized metrics that reduce greenwashing risk. |

| Avoid siloing your capital | Embedding impact across the full portfolio reduces risk and improves alignment with long-term goals. |

Why I think the philanthropy-versus-investing debate misses the point

The framing of philanthropy versus impact investing has always frustrated me. It implies a competition where none exists. The real question is not which tool is better. It is which tool fits the problem in front of you.

I have watched well-intentioned donors pour grant funding into organizations that were structurally ready for investment capital. The grants kept them dependent. I have also seen impact investors push commercial terms onto early-stage social enterprises that needed patient, concessional capital first. Both mistakes stem from the same error: treating the tool as the strategy rather than the outcome.

Many mission-driven organizations excel at articulating their impact but lack the financial governance and readiness to attract investment. That gap is not a failure of ambition. It is a structural problem that philanthropic capacity-building capital is uniquely positioned to solve. The subsidy gap in impact-first investing is real, and philanthropy is the most efficient tool for closing it.

My practical advice: stop asking whether you are a philanthropist or an impact investor. Start asking what stage of capital your target organizations actually need, and deploy accordingly. That shift in framing produces better outcomes than any ideological commitment to one approach over the other.

— Charles

Verdantinstitute courses for impact investors and donors

Knowing the theory is one thing. Building the skills to execute across the full capital continuum is another. Verdantinstitute offers structured learning tracks covering impact investing strategies and ESG analysis, designed for finance professionals and students who want to move from curiosity to competence.

The platform's library of 16 courses and over 160 lessons covers everything from foundational ESG concepts to advanced transition finance and net-zero strategies. CPD tracking and certifications make it practical for professionals who need to demonstrate skills to employers or clients. Plans start at $18 per month for students and $58 per month for professionals. If you are serious about deploying capital with both financial and social intent, the course catalog is a direct path to the technical fluency this work demands.

FAQ

What is the main difference between impact investing and philanthropy?

Impact investing targets measurable social or environmental outcomes alongside a financial return, while philanthropy delivers capital as grants or donations with no repayment expectation. The financial return requirement is the defining structural difference.

Can impact investing replace philanthropy?

Impact investing cannot replace philanthropy. Many high-impact social enterprises require catalytic grant capital before they are ready for investment, and Miller Center research shows the impact-first premium alone requires philanthropic funding to make deals viable.

What is venture philanthropy?

Venture philanthropy is a hybrid model combining grant funding with organizational capacity support, typically over a 3–7 year period, to help social enterprises become financially self-sustaining. It sits between traditional philanthropy and impact-first investing on the capital continuum.

How is impact measured in impact investing?

Impact investing uses standardized frameworks including IRIS+ and the Impact Management Project to track quantitative metrics such as jobs created, CO2 avoided, and affordable units delivered. Effective measurement requires iterative feedback loops, not just annual reporting.

What does "impact-first investing" mean?

Impact-first investing accepts below-market financial returns to reach projects that commercial capital will not fund. Research shows this approach carries an approximate $0.13 per dollar premium, which catalytic philanthropic capital is typically used to cover.