Thematic ESG investing is defined as an investment approach that targets specific sustainability themes, such as decarbonization, water scarcity, or the circular economy, while applying environmental, social, and governance (ESG) criteria to select and manage holdings. The industry term you will encounter in professional settings is "thematic sustainable investing," though the concept is the same. ESG integration remains the most widely adopted strategy, used by 77% of U.S. firms, but thematic ESG is growing fast as a targeted, opportunity-seeking complement. That distinction matters: thematic ESG does not simply screen out bad actors. It actively positions portfolios to capture long-term structural shifts, typically requiring a 5 to 10+ year investment horizon to let macro-level trends fully materialize. For finance professionals building sustainable portfolios in 2026, understanding where thematic ESG fits, and where it does not, is the starting point for every allocation decision.

What is thematic ESG investing and how does it differ from other ESG strategies?

Thematic ESG investing occupies a distinct position within the broader family of ESG investment strategies. Understanding that position requires comparing it directly with the three other dominant approaches: ESG integration, exclusionary screening, and impact investing.

ESG integration embeds environmental, social, and governance factors into traditional financial analysis to manage risk. A portfolio manager using ESG integration might downgrade a company's valuation because of poor governance scores, but the portfolio itself has no particular thematic focus. Thematic ESG, by contrast, starts with a macro-level trend and then applies ESG criteria to identify the best-positioned companies within that trend.

Exclusionary screening removes companies or sectors that fail ESG thresholds, such as tobacco producers or weapons manufacturers. It is a negative filter. Thematic ESG is a positive filter: it seeks companies that actively benefit from a sustainability transition, not just companies that avoid harm.

Impact investing targets measurable, intentional social or environmental outcomes, often in private markets. Thematic ESG funds operate primarily in public equity and fixed income markets, making them more liquid and accessible than most impact vehicles. The overlap exists when thematic funds apply strict ESG overlays and report on sustainability outcomes, but the primary objective remains financial return within a thematic lens. For a direct comparison of these approaches, the impact investing vs. ESG integration framework is a useful reference.

The practical implication for portfolio construction is concentration risk. Because thematic funds focus on a narrow slice of the economy, they carry higher sector and factor exposures than broad ESG integration strategies. A clean energy fund, for example, will have significant exposure to interest rate sensitivity and policy risk, regardless of how well the underlying companies score on ESG metrics.

Pro Tip: When evaluating a thematic ESG fund, check the fund's active share relative to a broad market index. Low active share signals the fund is closet-indexing rather than delivering genuine thematic exposure.

How to build a thematic ESG portfolio

Portfolio construction for thematic ESG investing requires a different mental model than traditional sector allocation. Thematic investing themes span multiple sectors, meaning a single theme like "smart cities" touches real estate, technology, utilities, and industrials simultaneously. That cross-sector nature makes traditional asset allocation frameworks inadequate on their own.

The standard professional approach is the core-and-satellite model. Financial planners recommend allocating 40–70% to broad-market core holdings and 20–40% across 3–6 thematic satellite positions. That structure preserves diversification at the portfolio level while allowing concentrated thematic bets to drive differentiated returns. The core provides stability; the satellites provide the opportunity.

Building the satellite layer effectively requires four steps:

- Define the theme with precision. "Clean energy" and "energy transition" sound similar but capture different companies. A fund focused on solar panel manufacturers differs materially from one focused on grid infrastructure. Specificity at this stage prevents unintended overlaps later.

- Run a look-through analysis. Because themes cross sectors, you must examine actual holdings rather than relying on fund labels. Look-through analysis is necessary to verify real exposure and avoid unintended market beta concentrations, particularly in mega-cap technology stocks that appear across multiple themes.

- Combine uncorrelated themes. Blending themes driven by uncorrelated economic drivers, such as pairing a policy-driven clean energy theme with a demographic-driven healthcare innovation theme, reduces portfolio volatility without diluting conviction in either trend.

- Cap thematic exposure. Experienced investors limit thematic allocations to below 20% of total equity exposure to control concentration risk and avoid the performance drag that comes from over-betting on a single structural trend.

A more advanced construction method treats ESG as a core optimization dimension alongside risk and return. 3D investing applies multi-objective optimization to build portfolios on an efficient frontier that accounts for ESG scores, financial risk, and expected return simultaneously. This approach produces more efficient thematic ESG portfolios than simply applying ESG as a post-construction filter.

Pro Tip: Map each thematic satellite to its primary economic driver, whether policy, demographics, technology adoption, or resource scarcity. If two satellites share the same driver, they will likely correlate during stress periods and reduce your diversification benefit.

What are the key benefits and risks of thematic ESG investing?

The primary benefit of thematic ESG investing is the potential to capture long-term alpha from structural trends that traditional sector-based portfolios miss. Decarbonization, water security, and the circular economy are not cyclical themes. They are driven by regulatory mandates, resource constraints, and shifting consumer behavior. Companies positioned at the center of these transitions have a multi-decade growth runway that short-term earnings analysis tends to undervalue.

ESG integration within thematic funds adds a second layer of benefit: risk management. Companies with strong ESG profiles tend to face fewer regulatory penalties, supply chain disruptions, and governance failures. When a thematic fund applies rigorous ESG criteria on top of thematic alignment, it filters out companies that are exposed to a trend but poorly managed, which is a real and common problem in early-stage sustainability sectors.

The risks are equally concrete:

- Concentration risk. Thematic funds hold fewer companies than broad market funds. A single regulatory reversal or technology disruption can hit a large portion of the portfolio at once.

- Theme overlap. Multiple thematic satellites can share the same underlying holdings, particularly large-cap technology companies. This creates hidden correlation that only appears during drawdowns.

- Greenwashing. Not all ESG-themed funds deliver true impact. Investors must scrutinize whether a fund's holdings genuinely align with the stated theme or simply carry an ESG label for marketing purposes.

- Market timing temptation. Thematic trends attract attention at peak valuations. Investors who enter after a theme has been widely publicized often buy at elevated multiples and underperform.

Rigorous due diligence is the non-negotiable prerequisite for thematic ESG investing. Investors must verify that a fund's core business holdings authentically align with the chosen sustainability theme and that credible ESG oversight governs the selection process. A fund name is not evidence of thematic alignment.

The long-term ESG performance evidence supports the thesis that ESG-integrated portfolios outperform over full market cycles. Thematic ESG funds that maintain both genuine thematic focus and strong ESG credentials are best positioned to capture that outperformance.

How can investors effectively implement thematic ESG strategies?

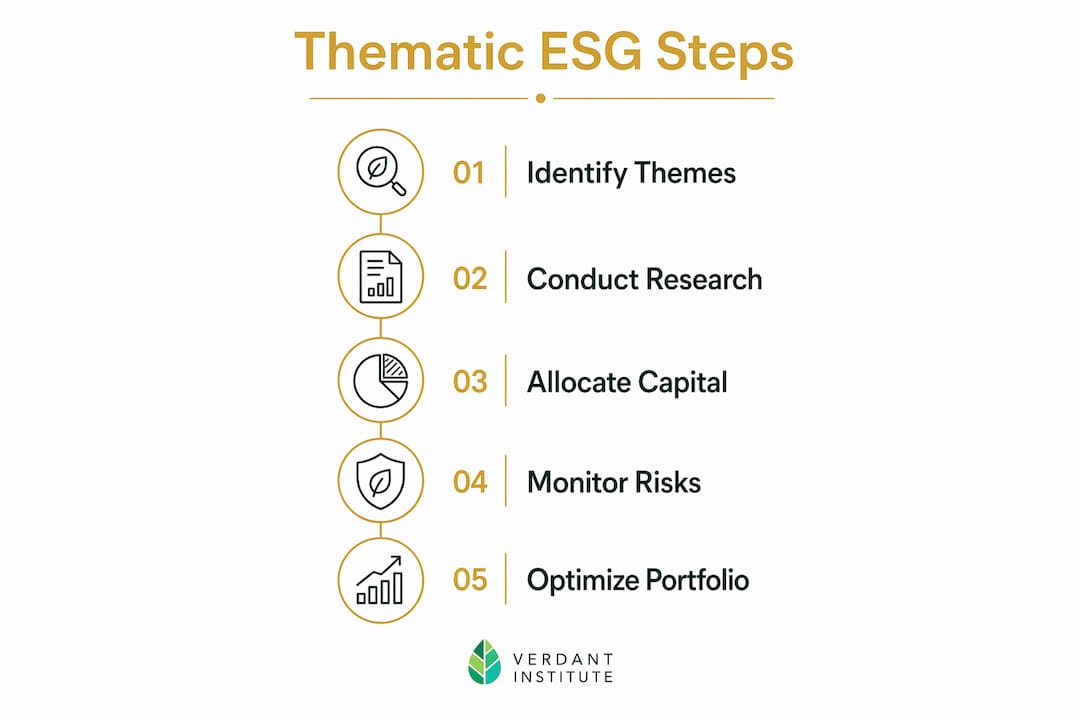

Effective implementation of thematic ESG investing follows a structured process. Ad hoc theme selection based on recent headlines is the fastest route to poor outcomes.

- Start with theme validation. Confirm that the theme is driven by a durable structural force, not a short-term narrative. Regulatory tailwinds, demographic shifts, and resource constraints qualify. Speculative technology cycles generally do not.

- Conduct ESG and thematic due diligence simultaneously. Evaluate each fund on two dimensions: the credibility of its ESG oversight process and the authenticity of its thematic alignment. Investors must perform rigorous due diligence to confirm that holdings' core businesses genuinely serve the chosen sustainability theme.

- Commit to the investment horizon. Thematic ESG strategies require patience. Structural trends unfold over years, not quarters. Investors who exit after 18 months of underperformance typically miss the compounding phase that justifies the initial thesis.

- Blend themes deliberately. Select 3–6 thematic satellites with distinct economic drivers. Pair policy-driven themes with technology adoption themes and demographic themes to build resilience across different macro environments.

- Combine thematic funds with broad ESG integration. Thematic ESG works best as a satellite allocation within a portfolio that also includes broad ESG integration in asset allocation. The integration layer provides baseline diversification; the thematic layer provides differentiated return potential.

- Review and rebalance annually. Sustainability trends evolve. A theme that was nascent in 2020 may be mainstream by 2026, reducing its alpha potential. Annual reviews allow you to rotate toward earlier-stage themes before they are fully priced in.

The practical discipline here is avoiding the two most common pitfalls: overconcentration and market timing. Both errors stem from treating thematic ESG as a tactical trade rather than a structural allocation. The investors who generate consistent results treat thematic positions the same way they treat any long-duration asset: with conviction, patience, and a clear exit thesis tied to theme maturation rather than price movement.

Key Takeaways

Thematic ESG investing generates its strongest results when used as a deliberate satellite allocation within a diversified portfolio, grounded in rigorous due diligence and a long-term investment horizon.

| Point | Details |

|---|---|

| Definition is precise | Thematic ESG combines sustainability theme targeting with ESG criteria, not just screening or broad integration. |

| Core-and-satellite structure | Allocate 40–70% to broad-market core holdings and 20–40% across 3–6 thematic satellites. |

| Look-through analysis is required | Themes cross sectors, so examining actual holdings is necessary to avoid hidden concentration. |

| Blend uncorrelated themes | Pair policy-driven and demographic-driven themes to reduce volatility without losing conviction. |

| Due diligence is non-negotiable | Verify authentic thematic alignment and credible ESG oversight before committing capital to any fund. |

Why thematic ESG deserves more scrutiny, not less enthusiasm

The finance industry has a well-documented tendency to package trends into products faster than investors can evaluate them. Thematic ESG is not immune to that dynamic. I have seen portfolios labeled "sustainable" that held the same 20 mega-cap technology stocks across four different thematic funds, with virtually no genuine thematic differentiation and minimal ESG rigor. The label was doing the work that the portfolio construction should have done.

The investors I respect most in this space treat thematic ESG as a complement to broad ESG integration, not a replacement. They use it to express high-conviction views on structural transitions, but they keep those positions sized appropriately and they do the unglamorous work of look-through analysis before committing capital. The 3D investing framework, which treats ESG as a core optimization variable alongside risk and return, represents the direction the field is moving. Investors who adopt that mindset now will be better positioned as sustainability factors become more deeply embedded in mainstream portfolio theory. Thematic ESG is not a fad. But it requires the same analytical discipline as any other concentrated bet, and the investors who treat it as a shortcut to impact will consistently underperform those who treat it as a craft.

— Charles

Build your thematic ESG knowledge with Verdantinstitute

Verdantinstitute offers structured ESG education built specifically for finance professionals who need more than surface-level familiarity with sustainable investing concepts.

The platform's Deep Dive and Advanced Practice learning tracks cover thematic sustainable investing, portfolio construction, and transition finance in depth. With over 160 lessons across 16 courses, CPD tracking, and certifications, Verdantinstitute gives professionals the analytical foundation to evaluate thematic ESG funds with confidence. Plans start at $18 per month for students and $58 per month for professionals. Visit Verdantinstitute's learning platform to review the full course catalog, or check the pricing and plan options to find the right fit for your professional development goals.

FAQ

What is thematic ESG investing in simple terms?

Thematic ESG investing means building a portfolio around specific sustainability trends, such as clean energy or water scarcity, while applying ESG criteria to select the strongest companies within those trends. It targets long-term structural shifts rather than broad market exposure.

How does thematic ESG differ from ESG integration?

ESG integration embeds ESG factors into financial analysis to manage risk across a broad portfolio, while thematic ESG focuses capital on companies that directly benefit from a specific sustainability transition. The two approaches are complementary and work best when combined.

What investment horizon does thematic ESG require?

Thematic ESG strategies typically require a 5 to 10+ year horizon because structural sustainability trends unfold over decades, not quarters. Investors who exit early frequently miss the compounding phase that justifies the initial thesis.

How much of a portfolio should go into thematic ESG?

Experienced investors cap thematic allocations below 20% of total equity exposure to control concentration risk. The core-and-satellite model allocates 20–40% of the portfolio to thematic satellites spread across 3–6 distinct themes.

How do I avoid greenwashing in thematic ESG funds?

Verify that the fund's actual holdings align with the stated sustainability theme by running a look-through analysis of the underlying positions. Confirm that the fund applies credible ESG oversight criteria, not just a sustainability label, before committing capital.