The best-in-class ESG approach is defined as a method of selecting companies by ranking them against industry peers on material environmental, social, and governance criteria to identify top performers. Unlike exclusionary strategies that remove entire sectors, this method keeps portfolios diversified while directing capital toward firms that manage sustainability risks better than their competitors. Frameworks like the Sustainability Accounting Standards Board (SASB) materiality standards and the IFRS Sustainability Disclosure Standards give practitioners the sector-specific tools to make those rankings credible. For finance professionals and sustainability practitioners, understanding what is best-in-class ESG approach means recognizing it as a relative performance standard, not an absolute purity test. The result is a strategy that rewards ESG leadership within every industry, including ones that some investors find controversial.

What is the best-in-class ESG approach, and how does it work?

The best-in-class ESG approach ranks companies against peers on ESG criteria within sectors to select top performers, maintaining diversification while focusing capital toward better sustainability risk managers. That peer-relative structure is what separates it from negative screening, which simply removes industries from consideration. A mining company, for example, can qualify for a best-in-class portfolio if it outperforms other mining companies on water management, safety records, and board independence.

The approach also accepts a nuance that many practitioners overlook. Best-in-class identifies relative leaders and is not equivalent to absolute sustainability. High-impact sectors can be included if they outperform peers on material factors. That distinction matters when communicating strategy to stakeholders who expect ESG to mean "clean" companies only.

Materiality is the engine that makes the rankings meaningful. SASB standards identify which ESG issues are financially material for each of 77 industry categories. Applying sector-specific materiality prevents a generic ESG score from penalizing an oil company for water use while ignoring the governance failures that actually drive its financial risk.

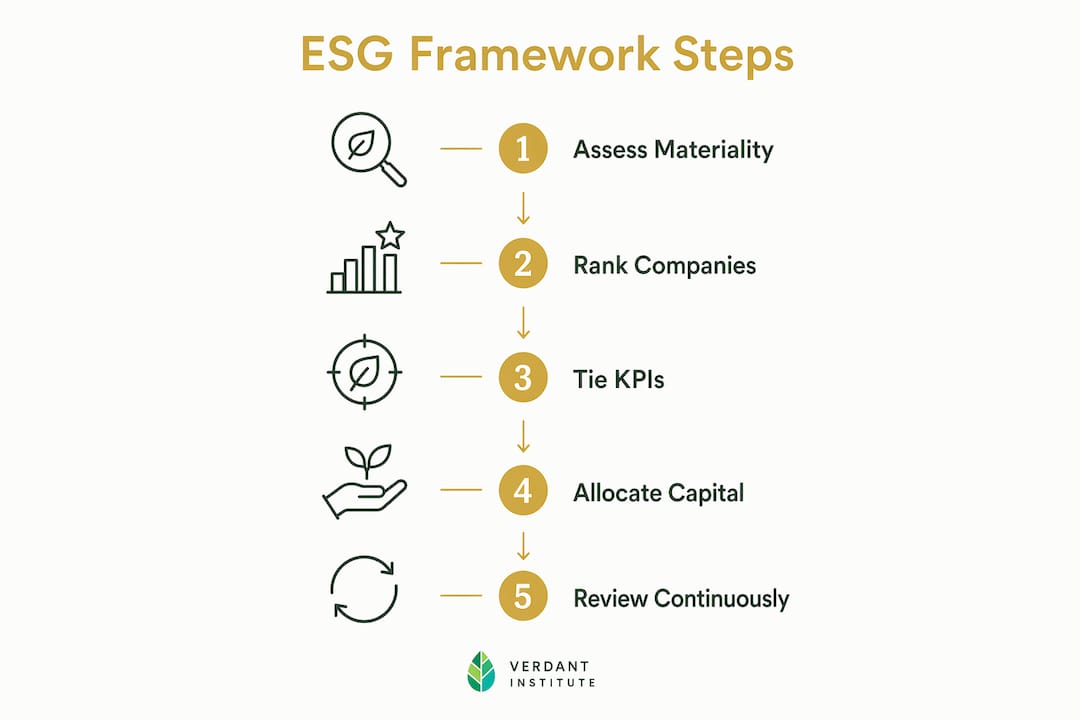

How to implement a best-in-class ESG framework

A structured implementation follows five stages: materiality assessment, leadership accountability, execution, data transparency, and risk management. Each stage builds on the previous one, so skipping the materiality step produces rankings that measure the wrong things.

-

Materiality assessment. Use SASB or the IFRS S1 and S2 standards to identify which ESG topics are financially significant for each sector in your portfolio or supply chain. Double materiality is now the gold standard, combining a financial lens with an impact lens to capture both investor risk and societal effect.

-

Leadership accountability. Assign named executives to ESG targets. Programs without board-level ownership stall at the reporting stage. Governance integration means ESG metrics appear in executive compensation frameworks, not just sustainability reports.

-

Execution. Translate material ESG topics into measurable KPIs with annual targets. Capital allocation decisions should reflect those KPIs. A company that sets a Scope 1 reduction target but funds no capital projects to achieve it has an execution gap, not an ESG strategy.

-

Data transparency. Third-party assurance of ESG data is the credibility threshold. Commitments backed by rigorous data and third-party assurance hold up better against greenwashing scrutiny, elevating program credibility. Assurance-ready data requires centralized collection systems, not spreadsheets distributed across business units.

-

Risk management. Embed ESG factors into the same risk registers used for financial and operational decisions. Embedding ESG into risk registers and decision-making frameworks used for finance and operations is key to achieving best-in-class performance.

Pro Tip: Tie ESG KPIs directly to capital allocation reviews. When ESG performance affects where the company invests, it stops being a reporting exercise and starts driving real decisions.

How do you handle ESG data challenges?

ESG data quality is the most common reason best-in-class programs fail to deliver credible outcomes. The core problem is rating divergence. ESG rating providers often disagree due to differing methodologies, which means an absolute score from one provider can contradict a score from another. Percentile rankings within industries are more reliable than absolute scores in best-in-class approaches because they normalize for methodology differences.

Practitioners face several specific data challenges:

- Decentralized supplier data. Scope 3 emissions and supply chain labor data rarely sit in one system. Collecting it requires structured supplier engagement programs, not one-off questionnaires.

- Assurance readiness. Data collected informally cannot be third-party verified. Building assurance-ready systems from the start saves significant rework later.

- Continuous due diligence. Due diligence in ESG must be continuous, not one-off, with Scope 3 targets and annual reporting required for suppliers exceeding 40% of total emissions. Periodic audits miss the performance drift that happens between review cycles.

- Supplier scorecards and corrective action. Effective programs use automated scorecards with defined escalation paths. Operationalizing strategy requires contractual ESG rights, defined escalation paths, and automation to avoid reliance on ineffective ad hoc questionnaires.

- Progress tracking over time. Point-in-time assessments show a snapshot. Trajectory data shows whether a company is improving, stalling, or declining.

Pro Tip: When evaluating suppliers or portfolio companies, weight improvement trajectories more heavily than current scores. A company moving from the 40th to the 65th percentile in two years is a stronger ESG bet than one sitting at the 70th percentile with no upward movement.

How does best-in-class ESG compare to other strategies?

Finance professionals working across types of ESG investment strategies need to position best-in-class accurately within the broader toolkit. Each method serves a different purpose, and mixing them up leads to misaligned mandates.

| Strategy | Core method | Key benefit | Main limitation |

|---|---|---|---|

| Negative screening | Excludes sectors or companies based on ESG violations or controversial activities | Simple to implement and communicate | Reduces diversification; misses leaders within excluded sectors |

| Best-in-class (positive screening) | Selects top ESG performers within each sector | Maintains diversification; rewards relative leadership | Includes high-impact sectors; requires robust data infrastructure |

| ESG integration | Systematically includes ESG factors in financial analysis and valuation | Applies to all asset classes; improves risk-adjusted returns | Depends on analyst judgment; inconsistent application |

| Thematic investing | Targets specific ESG themes such as clean energy or water | Direct exposure to sustainability trends | Concentrated sector risk; limited universe |

| Impact investing | Seeks measurable positive social or environmental outcomes alongside financial returns | Clearest link between capital and real-world change | Harder to scale; illiquidity in many vehicles |

Best-in-class ESG selects top-rated companies within sectors, while laggard or exclusionary strategies exclude based on poor ESG performance or controversial activities. The practical difference is that best-in-class allows a portfolio to hold energy companies, banks, or manufacturers, as long as those companies lead their peer group on material ESG criteria. A best-in-class approach allows holding companies in sectors some investors find objectionable, rewarding relative ESG leadership rather than absolute sustainability purity.

How to embed best-in-class ESG into daily workflows

Embedding best-in-class ESG into finance and sustainability workflows requires structural changes, not just reporting upgrades. The following practices move ESG from a compliance function to a core decision-making input.

- Board-level governance. Assign a board committee or named director responsibility for ESG oversight. Without governance accountability at the top, ESG targets lack enforcement.

- Capital allocation alignment. Review ESG performance data during capital budgeting cycles. Projects that worsen material ESG metrics should face a higher hurdle rate or require mitigation plans. Verdantinstitute's guidance on ESG in asset allocation outlines how to structure that review process.

- Supply chain due diligence. Embed contractual ESG rights into supplier agreements. Define what triggers an escalation, what corrective action looks like, and what constitutes grounds for disqualification.

- Data dashboards and feedback loops. Build dashboards that track ESG KPIs monthly, not annually. Annual reporting cycles are too slow to catch performance drift before it becomes a material risk.

- Transparent stakeholder reporting. Publish ESG performance data with third-party assurance statements. Transparency builds credibility with investors, regulators, and customers simultaneously.

- Ongoing program refinement. ESG value comes from measurable improvement trajectories across supplier and internal assessments rather than point-in-time screening alone. Schedule quarterly reviews to assess whether targets remain material and whether data collection methods remain fit for purpose.

For practitioners looking to sharpen their technical skills in this area, Verdantinstitute's resource on embedding ESG in investment decisions provides a structured framework for translating these principles into daily investment workflows.

Key Takeaways

The best-in-class ESG approach delivers durable results only when materiality, governance accountability, and continuous data improvement work together as a system.

| Point | Details |

|---|---|

| Relative ranking, not absolute purity | Best-in-class selects sector leaders on material ESG criteria, not companies free of all ESG risk. |

| Double materiality is the foundation | Use SASB or IFRS standards to identify which ESG issues are financially and socially material per sector. |

| Percentile ranks beat absolute scores | ESG rating divergence across providers makes industry percentile rankings more reliable for comparisons. |

| Continuous due diligence is required | One-off audits miss performance drift; effective programs track improvement trajectories over time. |

| Governance integration drives outcomes | ESG targets without board accountability and capital allocation linkage remain reporting exercises only. |

Why most ESG programs stall before they become best-in-class

The most common failure I see is treating ESG as a communications function. A team produces a polished sustainability report, the executive team approves it, and everyone moves on. Nothing in the risk register changes. Nothing in the capital budget changes. The program looks credible from the outside and delivers nothing on the inside.

Treating ESG as a checklist or communications-only function undermines true best-in-class performance. It must be woven into core risk and financial frameworks for impact. That means ESG data has to sit in the same systems that finance teams actually use, not in a separate sustainability platform that no one checks between reporting cycles.

The operational infrastructure challenge is real and underestimated. Building assurance-ready data systems, embedding contractual ESG rights into supplier agreements, and training procurement teams to use ESG scorecards takes 12 to 18 months of focused effort before it runs smoothly. Most organizations underestimate that timeline and then wonder why their program lacks credibility.

The practitioners who get this right share one habit: they measure improvement, not just current standing. A company at the 55th ESG percentile that has moved up 15 points in two years is building something real. A company at the 75th percentile with no upward movement is coasting on a legacy position that will erode. That distinction is what separates genuine ESG leadership from a well-managed reputation.

— Charles

Verdantinstitute: your next step in ESG mastery

Finance professionals and sustainability practitioners who want to move from ESG theory to applied practice need more than frameworks. They need structured training that connects materiality assessment, data governance, and governance integration into a single, coherent skill set.

Verdantinstitute offers a library of 16 courses and over 160 lessons covering foundational ESG concepts through advanced topics like transition finance and net-zero strategies. CPD tracking and certifications make the learning count toward professional development requirements. Plans start at $18 per month for students and $58 per month for professionals. Visit Verdantinstitute to find the learning track that fits your current role and your next career move.

FAQ

What is the best-in-class ESG approach in simple terms?

The best-in-class ESG approach selects companies that rank highest among their industry peers on material environmental, social, and governance criteria. It rewards relative ESG leadership within sectors rather than excluding entire industries.

How does best-in-class ESG differ from negative screening?

Negative screening removes sectors or companies based on ESG violations or controversial activities. Best-in-class keeps all sectors eligible and selects the top ESG performers within each one, preserving portfolio diversification.

Why do ESG ratings vary so much across providers?

ESG rating providers use different methodologies, weightings, and data sources, which produces significant divergence in scores for the same company. Percentile rankings within an industry are more reliable than absolute scores for best-in-class comparisons.

What frameworks support a best-in-class ESG materiality assessment?

SASB standards cover 77 industry categories and identify which ESG issues are financially material for each. The IFRS S1 and S2 standards add a double materiality lens that captures both financial risk and real-world impact.

How often should a best-in-class ESG program be reviewed?

Effective programs run continuous due diligence rather than annual audits. Quarterly reviews of ESG KPIs and supplier scorecards catch performance drift early and keep improvement trajectories on track.