Impact investing risk is defined as the probability that targeted social or environmental outcomes fail to materialize as expected, creating a layer of uncertainty that sits entirely outside traditional financial risk models. This distinction matters because how impact investing works requires investors to manage two parallel risk dimensions simultaneously: financial return uncertainty and impact outcome uncertainty. Understanding why impact investing risk differs is not optional for serious practitioners. It is the foundation of credible due diligence, and 97% of investors identify measuring impact as a leading barrier to effective risk management. Frameworks like Impact Frontiers' Five Dimensions of Impact formalize this separation, treating impact risk as its own critical variable.

Why impact investing risk differs from standard financial analysis

Impact risk is defined as the likelihood that an investment's actual social or environmental outcomes diverge from what was projected at the time of commitment. This is not the same as financial risk, which concerns the probability of losing capital or missing return targets. The two can move independently. A fund can generate strong financial returns while completely failing its stated impact mission, and vice versa.

Traditional financial risk assessment relies on quantitative tools: volatility measures, credit ratings, scenario analysis, and stress testing. Impact risk assessment demands a different toolkit. Practitioners use the Five Dimensions of Impact, a framework developed by Impact Frontiers, which evaluates what outcomes are being achieved, for whom, how much, how deeply, and with what degree of contribution beyond what would have happened anyway. Each dimension carries its own uncertainty, and each must be assessed separately.

Due diligence for impact risk integrates both quantitative and qualitative methods. Quantitative approaches include impact multiples of money, which measure the social return generated per dollar invested. Qualitative methods include stakeholder interviews, Theory of Change reviews, and site assessments. Neither method alone is sufficient.

- Impact risk is distinct from financial risk. An investment can succeed financially while failing its mission entirely.

- The Five Dimensions of Impact provide a structured lens for assessing each source of impact uncertainty.

- Impact multiples of money translate social outcomes into measurable, comparable units.

- Impact covenants are enforceable contractual obligations that reduce the risk of impact non-delivery.

Pro Tip: Build impact risk criteria directly into your investment committee templates. If impact risk is assessed separately from financial risk and never reconciled, it will be ignored under time pressure.

How does liquidity risk compound the impact investing risk profile?

Impact portfolios carry a structurally different liquidity profile than traditional equity or fixed income portfolios. The concentration in private equity, venture capital, and private debt means that exit options are limited and often depend on market conditions outside the investor's control. This is not a temporary feature. It is a design characteristic of the asset classes most commonly used to generate deep impact.

Impact AUM grew 21% annually, yet IPO volumes remain well below 2021 levels. That gap matters because private equity impact funds depend on public market exits to return capital to investors. When IPO windows close, holding periods extend, and liquidity risk compounds. Investors who modeled a seven-year fund life may find themselves in year ten with no clear exit path.

Closed-ended fund structures make this worse. Investors commit capital for a fixed term with no ability to redeem early. The impact investing asset classes most associated with deep social outcomes, such as affordable housing, early-stage health technology, and agricultural development, are precisely those with the thinnest secondary markets.

The tradeoff between liquidity and impact is real and must be priced into portfolio construction decisions from day one.

- Assess your liquidity horizon first. Impact portfolios with heavy private market exposure require patient capital commitments of seven to twelve years.

- Model exit scenarios under stress. Assume IPO markets remain depressed and build secondary sale assumptions into your base case.

- Diversify across fund vintages. Staggering commitments across multiple years reduces the risk of all exits clustering in a single market environment.

- Reserve liquidity buffers. Institutional investors should maintain liquid reserves to meet capital calls without forced selling elsewhere in the portfolio.

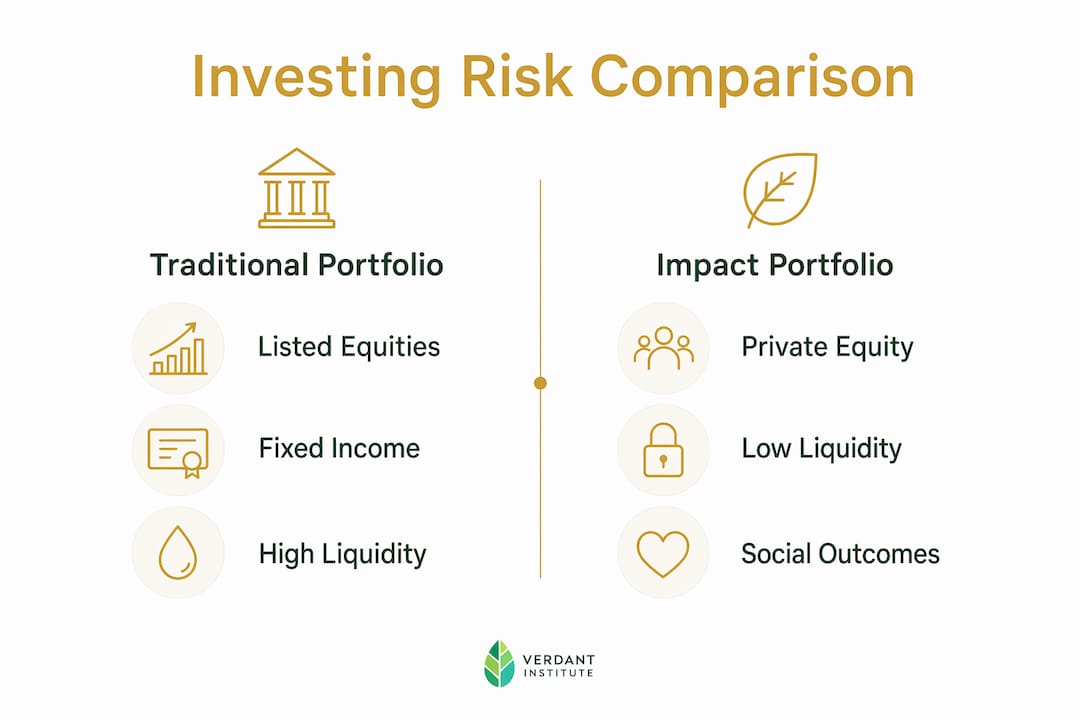

| Risk factor | Traditional portfolio | Impact portfolio |

|---|---|---|

| Primary asset class | Listed equities, bonds | Private equity, venture capital |

| Typical liquidity | Daily to monthly | Seven to twelve years |

| Exit dependency | Public markets | IPOs, secondary sales, trade buyers |

| Liquidity risk driver | Market volatility | IPO volume, secondary market depth |

Pro Tip: When evaluating a closed-ended impact fund, ask the GP for a detailed exit strategy for each portfolio company. Vague answers on exit planning are a leading indicator of liquidity risk being underestimated.

How does impact risk interact with financial returns?

The assumption that impact investing always requires accepting lower financial returns is wrong. Listed impact equities outperformed benchmarks by 5.2% annually and showed shallower drawdowns during volatile markets. That data directly challenges the concessionary return narrative that has dominated the field for years.

That said, impact-first investments do sometimes involve deliberate financial concessions. The key word is deliberate. Concessions are valid when they are transparent, justified by measurable outcomes, and supported by operational safeguards. A concessionary return accepted without a clear Theory of Change and measurable impact targets is not impact investing. It is philanthropy with a return expectation attached.

Operational risk is a separate but related concern. Smaller impact funds often lack the governance infrastructure of large institutional managers. Weak board oversight, inadequate financial controls, and high staff turnover all increase the probability that impact targets are missed, not because the mission is flawed, but because execution fails.

"Impact-first risk is often a deliberate design feature with transparent tradeoffs, not a sign of inferior investment quality. The distinction between intentional concession and poor investment management is the most important judgment call in impact due diligence."

The practical implication is that finance professionals must evaluate operational integrity as a core component of impact risk assessment, not as an afterthought.

What institutional standards exist to manage impact risk?

The Operating Principles for Impact Management, developed under the auspices of the International Finance Corporation, require signatories to conduct ex-ante impact risk assessments before committing capital. The standard is clear: impact risk must be identified, assessed, and linked to real decision thresholds before an investment closes. Inconsistent ex-ante assessment leads to overstated impact ambitions and weak risk mitigation in practice.

Theory of Change maintenance is a critical and frequently neglected tool. A Theory of Change maps the causal pathway from investment activity to social or environmental outcome. When it is not updated as market conditions change, the due diligence logic becomes stale. Disconnected diligence stages cause institutional memory loss, meaning the team that manages the investment no longer understands the assumptions the team that made it relied on.

| Mitigation tool | What it does | Common failure mode |

|---|---|---|

| Ex-ante impact risk assessment | Identifies impact risks before commitment | Not linked to actual go/no-go decisions |

| Theory of Change | Maps causal pathway to outcomes | Not updated after initial investment |

| Impact covenants | Contractually enforces impact performance | Poorly defined metrics make enforcement weak |

| Impact multiples of money | Quantifies social return per dollar | Relies on assumptions that are rarely stress-tested |

| KPI reporting | Tracks ongoing impact delivery | Reporting frequency too low to catch drift early |

The sustainable finance frameworks that underpin these standards are not optional add-ons. They are the infrastructure that separates credible impact investing from impact washing.

Practical steps for integrating impact risk into investment decisions

Finance professionals who treat impact risk as a separate workstream from financial risk create a structural problem. The two must be integrated from the earliest stage of deal screening through to exit. Due diligence failures most often arise because screening, onboarding, and reporting are disconnected, not because the underlying investment was flawed.

The small allocation trap is a concrete example of how structural decisions undermine impact risk management. Allocating less than 5% of capital to impact investments creates under-resourcing that makes it nearly impossible to conduct thorough due diligence, maintain Theory of Change updates, or enforce impact covenants. The allocation is too small to justify the governance overhead, so it gets sidelined.

- Integrate impact and financial risk into a single due diligence process. Separate workstreams create gaps that neither team owns.

- Set a minimum allocation threshold. Commitments below 5% of total capital rarely generate the governance attention needed for effective impact risk management.

- Define impact KPIs before closing. Metrics agreed post-investment are almost always weaker than those negotiated as conditions of commitment.

- Schedule Theory of Change reviews annually. Treat them as a standing agenda item, not a one-time exercise.

- Use impact covenants as a standard term. Enforceable impact obligations shift accountability from aspiration to contractual requirement.

Balancing risk, impact ambition, and financial return requires transparent tradeoffs documented in the investment thesis. An impact investing thesis that does not explicitly address impact risk is incomplete, regardless of how strong the financial projections look.

Key Takeaways

Impact investing risk differs from traditional financial risk because it includes a distinct impact dimension that requires specialized frameworks, contractual safeguards, and integrated due diligence to manage effectively.

| Point | Details |

|---|---|

| Impact risk is a separate dimension | It measures the probability that social or environmental outcomes fail, independent of financial returns. |

| Liquidity risk is structurally elevated | Private equity and venture capital concentration creates seven to twelve year illiquidity that must be planned for explicitly. |

| Concessions require transparency | Deliberate return tradeoffs are valid only when tied to measurable outcomes and operational safeguards. |

| Institutional standards exist | The Operating Principles for Impact Management require ex-ante risk assessment linked to real investment decisions. |

| Integration prevents failure | Siloed due diligence and small allocations below 5% are the leading causes of impact risk management breakdown. |

Why impact risk demands a new analytical mindset

I have spent years watching finance professionals approach impact investing as though it were traditional investing with an ESG checklist bolted on. That framing is the root cause of most impact risk failures I have seen. The measurement challenge is real. When 97% of investors flag it as a barrier, that is not a data quality problem. It is a signal that the analytical frameworks most professionals were trained on simply do not apply.

What I find genuinely interesting is that properly managed impact risk becomes a catalytic asset rather than a liability. The discipline required to define a Theory of Change, set measurable KPIs, and enforce impact covenants forces a level of investment rigor that many traditional funds lack. Funds that do this well tend to have better governance, clearer exit strategies, and more honest conversations about risk tradeoffs.

The professionals who will lead this field are not those who minimize impact risk or treat it as a compliance exercise. They are the ones who treat it as a source of analytical edge. Understanding the Five Dimensions of Impact, knowing when a concessionary return is justified, and recognizing the small allocation trap before it derails a portfolio: these are the skills that separate credible impact investors from those who are simply following a trend.

— Charles

Build the skills to assess impact risk with confidence

Impact risk assessment requires a specific set of frameworks and analytical habits that most finance training programs do not cover. Verdantinstitute offers structured learning tracks built for finance professionals who need to go beyond ESG fundamentals and develop real competency in impact risk evaluation.

Verdantinstitute's curriculum covers the Five Dimensions of Impact, Theory of Change development, impact covenants, and the Operating Principles for Impact Management across more than 160 lessons. The professional plan at $58/month includes CPD tracking and certifications that demonstrate applied competency to employers and clients. Finance professionals who need foundational grounding before tackling advanced topics can start with the Foundations track and move into Deep Dives on specific risk areas. Review the Verdantinstitute pricing plans to find the right fit for your professional development goals.

FAQ

What is impact risk in investing?

Impact risk is the probability that an investment's social or environmental outcomes fail to materialize as expected. It is a distinct risk dimension, separate from financial risk, and requires its own assessment frameworks.

Why does impact investing risk differ from ESG investing risk?

Impact investing requires measurable, intentional outcomes tied to specific interventions, while ESG investing focuses on risk screening. Impact risk includes the possibility that targeted outcomes do not occur, which ESG analysis does not typically measure.

How do impact covenants reduce investment risk?

Impact covenants are enforceable contractual obligations that require investees to meet defined impact targets. They shift accountability from aspiration to legal requirement, reducing the risk of impact non-delivery.

What is the small allocation trap in impact investing?

The small allocation trap occurs when investors commit less than 5% of capital to impact investments. The allocation is too small to support proper due diligence, governance, or impact covenant enforcement.

Do impact investments always produce lower financial returns?

No. Listed impact equities have outperformed traditional benchmarks by 5.2% annually with shallower drawdowns. Concessionary returns are sometimes intentional and justified, but they are not an inherent feature of all impact investments.